Drug Discovery Outsourcing Market to Reach USD 6.81 Billion by 2032, Surging at 7.20% CAGR Amid AI Integration, Biologics Boom, and Strategic R&D Restructuring.

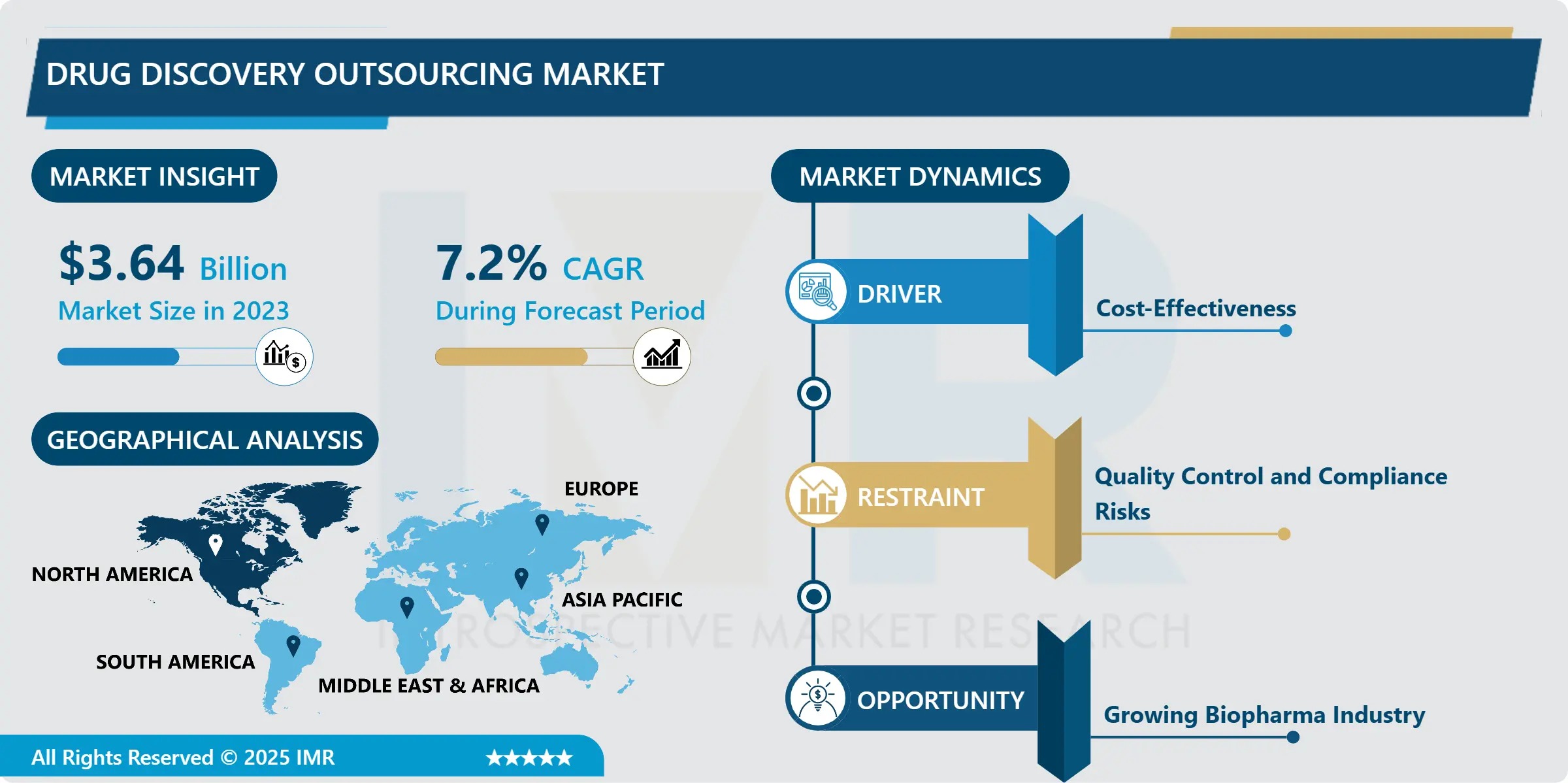

The Global Drug Discovery Outsourcing Market is entering a high-velocity growth phase, propelled by unprecedented pressure on pharmaceutical innovators to accelerate pipeline velocity while constraining ballooning R&D costs. According to Introspective Market Research’s latest analysis, the market-valued at USD 3.64 billion in 2023-is projected to reach USD 6.81 billion by 2032, expanding at a compound annual growth rate (CAGR) of 7.20% from 2024 to 2032. This robust trajectory reflects a fundamental shift in how drug development is conducted: from vertically integrated in-house operations to agile, modular, and technology-augmented ecosystems powered by specialized Contract Research Organizations (CROs), Contract Development and Manufacturing Organizations (CDMOs), and academic-industry consortia.

Key growth catalysts include the rising complexity of novel therapeutic modalities-including cell and gene therapies, RNA-based therapeutics, and multi-specific biologics-which demand niche expertise beyond the core competencies of many pharma firms. Simultaneously, the integration of artificial intelligence (AI) and high-throughput screening (HTS) platforms is dramatically improving hit rates and reducing preclinical failure-capabilities that CROs are deploying at scale and lower marginal cost. Regulatory harmonization (e.g., FDA’s Project Optimus, EMA’s Innovation Task Force) and evolving reimbursement models favoring precision medicine further incentivize early-stage partnerships with discovery specialists to de-risk clinical translation.

Quick Insights: Market Pulse at a Glance

• Market Size (2023): USD 3.64 billion

• Projected Market Size (2032): USD 6.81 billion

• CAGR (2024–2032): 7.20%

• Dominant Workflow Segment: Target Identification & Screening (largest revenue share)

• Fastest-Growing Segment: Lead Identification & Candidate Optimization (driven by AI-enabled molecular design)

• Leading Therapeutic Area: Oncology (over 28% of outsourced discovery activity)

• Top Region: North America (42% share in 2023), followed by Western Europe (29%)

• Key Outsourcing Model: Hybrid (targeted functional service provision + FSPs)

• Top Players: WuXi AppTec, Charles River, Evotec, Laboratory Corporation of America, GenScript, Syngene International, Pharmaron

Revenue Forecast by Key Workflow Segments (2023–2032)

Workflow Segment | 2023 Revenue (USD Mn) | 2028E Revenue (USD Mn) | 2032E Revenue (USD Mn) | CAGR |

|---|---|---|---|---|

Target Identification & Screening | 1,389.2 | 2,412.3 | 2,876.4 | 7.8% |

Target Validation & Functional Informatics | 728.1 | 1,267.5 | 1,524.2 | 7.1% |

Lead Identification & Candidate Optimization | 947.6 | 1,720.9 | 2,112.8 | 8.4% |

Preclinical Development & Associated Services | 575.1 | 1,024.2 | 1,297.6 | 6.5% |

Total | 3,640.0 | 6,424.9 | 6,811.0 | 7.20% |

Therapeutic Area Breakdown (2023 Share & Growth Outlook)

Therapeutic Area | 2023 Market Share | Key Drivers |

|---|---|---|

Oncology | 28.3% | Rise of immuno-oncology, tumor-agnostic targets, ADC & bispecific platforms |

Central Nervous System | 14.1% | AI-driven blood-brain barrier penetration modeling, novel tau & synuclein targets |

Immunomodulation | 12.7% | Expansion into autoinflammatory and fibrotic diseases; cytokine-focused libraries |

Anti-infective | 9.6% | AMR crisis spurring novel mechanism discovery (e.g., phage-lysins, CRISPR antimicrobials) |

Cardiovascular & Metabolic | 8.9% | GLP-1 analog diversification, RNA-targeted therapies for lipid disorders |

Can AI-Augmented Discovery Ecosystems Close the “Valley of Death” Between Target Validation and Clinical Proof-of-Concept?

The most transformative shift in drug discovery outsourcing isn’t just who does the work-it’s how it’s done. CROs and tech-enabled biotechs are now embedding generative AI, quantum-inspired molecular simulation, and automated lab robotics into core service offerings-turning months-long cycles into weeks. Consider these recent milestones:

- Evotec deployed its proprietary EVOlution AI™ platform in partnership with Sanofi to identify three novel GPCR modulators for metabolic disease in under 90 days-cutting typical lead identification timelines by 65%.

- WuXi AppTec launched DELopen™ 2.0, an open-access DNA-encoded library (DEL) screening service with >10 billion compound diversity and integrated AI deconvolution, reducing client hit-to-lead costs by 40%.

- Charles River integrated its Cognate BioServices AI engine with high-content imaging to predict off-target toxicity at the lead optimization stage-improving candidate attrition profiles by 31% in 2024 validation studies.

- Syngene International (Biocon Group) inaugurated India’s first fully automated Digital Biology Lab in Bengaluru, featuring robotic HTS, AI-based SAR modeling, and cloud-based data sharing-serving global innovators with 24/7 discovery capacity at 30% lower FTE cost.

Equally pivotal is the rise of fractional expertise: instead of full outsourcing, large pharma increasingly engages CROs for highly specific capabilities-e.g., cryo-EM structural validation (GenScript), organoid-based phenotypic screening (Oncodesign), or PROTAC ternary complex modeling (Jubilant Biosys). This “plug-and-play innovation” model minimizes fixed overhead while maximizing scientific optionality.

Dr. Priya Nayar, Principal Consultant for Discovery & Development Strategy at Introspective Market Research, states:

“The 7.2% CAGR understates the tectonic realignment underway. We’re seeing a bifurcation: commoditized screening services are growing at ~5%, while AI-integrated, modality-specific discovery-especially for biologics, RNA, and complex small molecules-is expanding at 12–15% annually. The winners are those CROs that function not as vendors, but as co-innovators-embedding themselves in the client’s strategic decision loops. Crucially, the economics are shifting: a fully outsourced early discovery program now costs ~USD 8–12 million per candidate, versus USD 22+ million in-house. For mid-cap biotechs with limited capital, that delta isn’t just efficient-it’s existential.”

Regional Deep Dive: North America Leads, But Asia-Pacific Emerges as the Innovation & Scale Engine

North America remains the undisputed hub, accounting for over 42% of global outsourcing spend in 2023. The U.S. dominance stems from its unparalleled concentration of venture-backed biotechs, NIH-funded academic centers, and regulatory-science leadership. The Inflation Reduction Act’s R&D tax credit enhancements (Section 41) and FDA’s Emerging Technology Program have further incentivized partnerships with CROs offering advanced analytics and continuous manufacturing integration. California, Massachusetts, and North Carolina-home to over 60% of U.S. biotechs-serve as discovery outsourcing hotspots, with local CRO ecosystems providing end-to-end support from target ID to IND-enabling studies.

Western Europe holds the second-largest share (29%), anchored by Germany’s strong chemical biology base (Evotec, Bayer collaborations), the UK’s AI-biotech nexus (BenevolentAI, Exscientia spinouts), and France’s public-private innovation clusters (Genopole, Lyonbiopôle). The EU’s Innovative Health Initiative (IHI) has committed €1.2 billion through 2027 to de-risk early-stage discovery—much of it channeled via CRO-academia consortia.

Asia-Pacific, while currently at 18% share, is the fastest-growing region (CAGR 9.1%), driven by strategic investments in India and China. India has emerged as the “discovery back office” of choice for global innovators, with Syngene, Jubilant, and TCG Lifesciences offering Western-quality science at 40–60% lower cost-bolstered by English fluency, IP-robust legal frameworks (India’s Patent (Amendment) Act 2024), and deep talent pools in computational chemistry and bioinformatics. Meanwhile, China’s Made in China 2025 initiative has catalyzed massive infrastructure build-out: WuXi AppTec and Pharmaron operate integrated campuses with >5,000 discovery scientists and automated platforms rivaling U.S. benchmarks.

Segment Spotlight: Target ID & Screening Leads, but Lead Optimization Is the New Battleground

The Target Identification & Screening segment commands the largest revenue share-understandably, as it’s the critical first filter in the funnel. Here, advances in multi-omics integration (spatial transcriptomics + CRISPR screening + proteomics) enable systems-level target prioritization. Companies like QIAGEN and Thermo Fisher provide end-to-end biomarker-to-target workflows, while CROs like Eurofins and LabCorp offer scalable phenotypic and target-based HTS.

However, the highest-value growth is in Lead Identification & Candidate Optimization, where AI is reshaping the economics. Traditional medicinal chemistry teams required 6–12 months to iterate 50–100 analogs; today, platforms like Insilico Medicine’s Pharma.AI or Recursion’s Recursion OS generate 1,000+ optimized leads in silico within weeks-prioritized by predicted ADMET, synthetic feasibility, and novelty scores. CROs are rapidly acquiring or partnering with such AI-native firms: Charles River’s acquisition of Distributed Bio (2023), and LabCorp’s strategic alliance with Valence Discovery (2024), exemplify this convergence.

Cost Pressures and the Path to Sustainable Discovery Economics

R&D productivity remains stubbornly low: only ~12% of Phase I candidates reach approval, with average development costs exceeding USD 2.3 billion per drug. In this context, outsourcing delivers four critical levers for cost efficiency:

- Scalable Talent-on-Demand: CROs provide surge capacity for time-bound projects (e.g., library synthesis, in vivo PK/PD) without long-term HR commitments-reducing fixed labor costs by 25–35%.

- Shared Infrastructure Utilization: High-end assets (cryo-EM, DEL screening, organ-on-chip) remain prohibitively expensive for single companies; CROs amortize CapEx across dozens of clients.

- AI-Driven Attrition Reduction: Predictive toxicology and polypharmacology modeling in lead optimization cut late-stage failures—saving up to USD 150 million per avoided Phase II flop.

- Geographic Arbitrage with Quality Assurance: Tier-2 CRO hubs in Eastern Europe (Poland, Czechia) and India now meet OECD GLP standards while offering 30–50% lower FTE rates than the U.S. or Germany.

The benefits extend beyond cost: companies that strategically outsource early discovery report 18–24 months faster time-to-IND and 2.3x higher portfolio diversification-critical in an era where therapeutic area concentration poses existential risk.

About the Report

“Drug Discovery Outsourcing Market Key Developments, Demand & Forecast Report (2024-2032)” delivers an exhaustive assessment of the evolving partner ecosystem. The report features 220+ data tables, 30+ company deep-dives, and proprietary analysis of 14 therapeutic areas, 4 workflow stages, and 7 regional markets. It includes exclusive interviews with discovery leads from Pfizer, AstraZeneca, and 10 emerging biotechs, plus scenario modeling on the impact of AI regulation (EU AI Act), U.S. CHIPS-and-Science funding for biofoundries, and China’s data localization policies on cross-border discovery collaboration.

👉 Download Sample Report: https://introspectivemarketresearch.com/request/20163

About Introspective Market Research

Introspective Market Research(IMR) is a globally recognized leader in life sciences intelligence, empowering pharmaceutical companies, biotechs, investors, and policymakers with data-driven foresight. Our team of 100+ analysts-comprising former FDA reviewers, medicinal chemists, AI ethicists, and ex-C-suite executives-combines deep therapeutic expertise with cutting-edge analytics to decode market evolution. Trusted by WHO, Gates Foundation grant recipients, and Fortune 500 R&D leaders, we deliver more than reports: we deliver decision advantage.

Media Contact:

Anika Patel

Director of Strategic Communications

Introspective Market Research.

Email: info@introspectivemarketresearch.com

Phone: +91 91753-37569.