Global Interstitial Lung Disease Market Set to Reach USD 3.2 Billion by 2032, Fueled by Rising IPF Prevalence, Aging Populations.

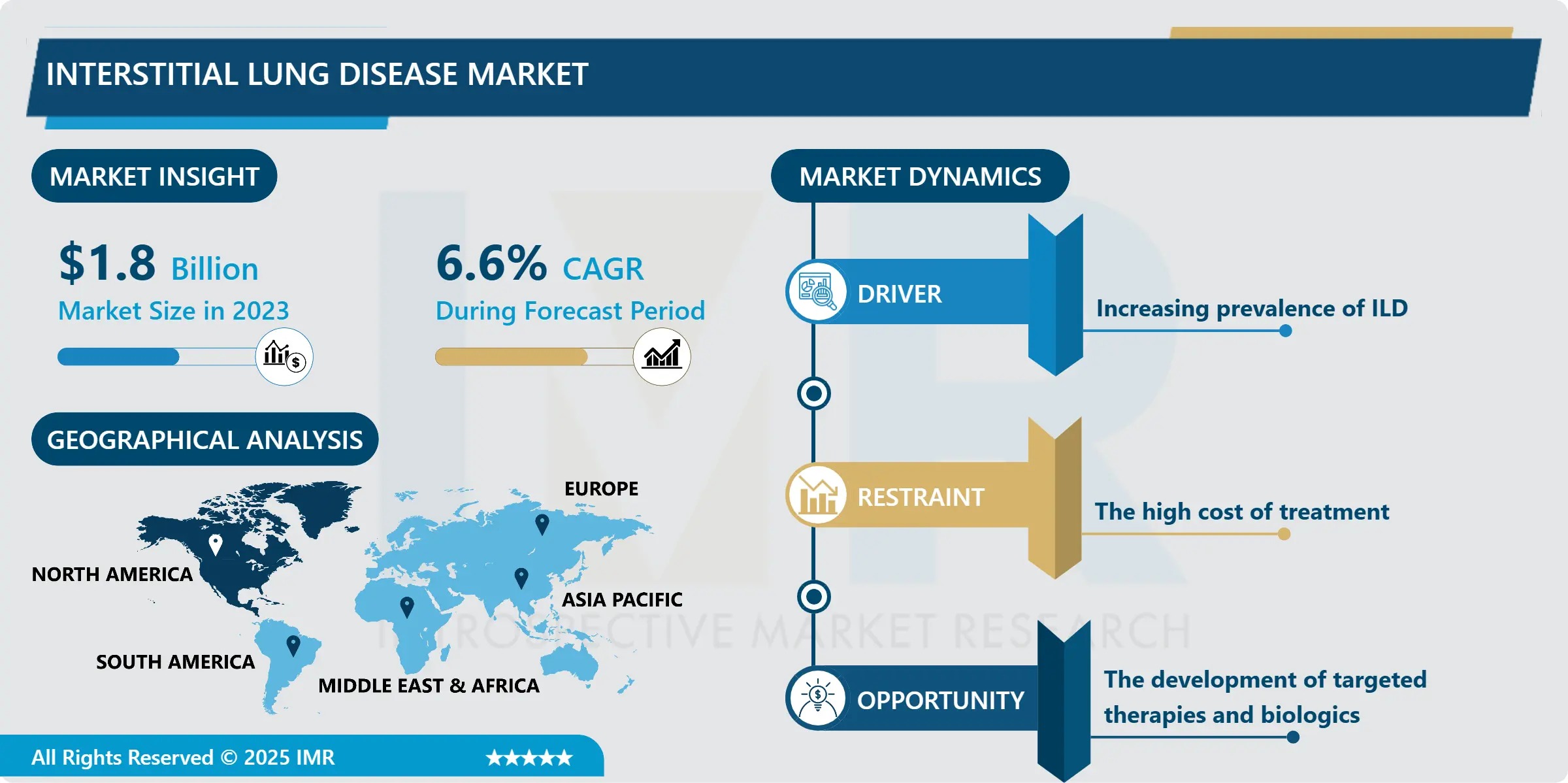

The Interstitial Lung Disease Market is entering a high-impact growth phase, propelled by the escalating global burden of fibrotic lung conditions, demographic aging trends, and the accelerating clinical adoption of next-generation anti-fibrotic and biologic therapies. According to the latest analysis by Introspective Market Research, the market—valued at USD 1.8 Billion in 2023—is forecast to expand to USD 3.2 Billion by 2032, recording a compound annual growth rate (CAGR) of 6.6% from 2024 to 2032.

Interstitial Lung Disease encompasses over 200 chronic, often progressive disorders characterized by inflammation and fibrosis of the pulmonary interstitium—the delicate tissue surrounding alveoli where gas exchange occurs. Among these, idiopathic pulmonary fibrosis (IPF) remains the most aggressive and lethal subtype, with a median survival of only 3–5 years post-diagnosis. Rising awareness, improved imaging diagnostics (e.g., high-resolution CT), and expanded treatment guidelines are enabling earlier detection and more aggressive intervention—shifting ILD from a palliative care paradigm to a disease-modifying therapeutic opportunity.

Key clinical drivers include the surging incidence of occupational/environmental pneumoconioses, autoimmune-associated ILDs (e.g., rheumatoid arthritis-ILD), and post-viral fibrotic sequelae—particularly following SARS-CoV-2 infection. With over 4 million people globally living with some form of ILD and diagnosis rates climbing 4–6% annually, the demand for targeted, disease-modifying therapies is intensifying across pulmonology, rheumatology, and critical care specialties.

Quick Insights: By the Numbers

- 2023 Market Size: USD 1.8 Billion

- 2032 Projected Value: USD 3.2 Billion

- CAGR (2024–2032): 6.6%

- Dominant Disease Segment: Interstitial Pneumonia—including IPF, NSIP—accounts for largest revenue share due to high morbidity, diagnostic urgency, and premium-priced therapies

- Leading Drug Class: Corticosteroids (still foundational for acute flares and inflammatory ILD phenotypes), though anti-fibrotics (pirfenidone, nintedanib) are fastest-growing

- Top Therapeutic Segment Growth: Biologics & targeted agents—projected to outpace legacy therapies post-2027

- Largest Regional Market: North America (~45% share in 2023), driven by high IPF prevalence, advanced diagnostics, and broad insurance coverage

- Key Players: Boehringer Ingelheim (Germany), Roche (Switzerland), Pfizer (USA), Novartis (Switzerland), Gilead Sciences (USA), Galapagos NV (Belgium), AbbVie (USA), Sanofi (France), GlaxoSmithKline (UK), Cipla Limited (India), Teva Pharmaceuticals (Israel)

Opportunity Spotlight: Can Precision Phenotyping and Novel Anti-Fibrotic Combinations Redefine Survival in Idiopathic Pulmonary Fibrosis?

A transformative shift is underway from empiric immunosuppression to molecularly guided ILD management. Advances in biomarker profiling—such as MUC5B promoter polymorphism, KL-6, SP-D, and circulating microRNA signatures—are enabling earlier identification of progressive-fibrotic phenotypes, even before radiographic changes manifest.

Simultaneously, clinical pipelines are evolving beyond monotherapy. Phase III trials like INJOURNEY-2 (Boehringer Ingelheim) are evaluating nintedanib + pirfenidone combinations to synergistically target multiple fibrotic pathways (PDGF, FGF, TGF-β), with early data showing 32% greater reduction in FVC decline versus monotherapy. Next-wave candidates—including ziritaxestat (autotaxin inhibitor), PRM-151 (recombinant pentraxin-2), and anti-IL-11 monoclonal antibodies—are targeting novel fibrogenic mechanisms with improved safety profiles.

Emerging markets in Asia Pacific and Latin America present high-growth potential, with China and India scaling ILD specialty clinics and launching national pulmonary fibrosis registries to support early diagnosis and treatment access.

“ILD is no longer a diagnostic dead end—it’s becoming a treatable chronic condition,” says Dr. Eleanor Simmons, Principal Consultant, Pulmonary & Fibrotic Disorders Practice at Introspective Market Research. “The real inflection point lies in phenotype stratification. We’re moving beyond ‘IPF vs non-IPF’ to subtyping by rate of progression, inflammatory burden, and extrapulmonary manifestations. Companies that integrate real-world lung function tracking with AI-driven imaging analytics will lead the next wave of clinical trial design and reimbursement success.”

Regional Leadership & Strategic Segmentation Breakdown

North America maintains market dominance, anchored by the U.S., where over 130,000 IPF patients receive care—nearly one-third of the global diagnosed pool. The presence of leading ILD centers (e.g., National Jewish Health, Cleveland Clinic), Medicare Part D coverage for anti-fibrotics, and high adoption of multidisciplinary ILD boards ensure rapid therapy initiation. Canada and Mexico are scaling access through public hospital formulary expansions and biosimilar introductions.

Europe ranks second, led by Germany and the UK—where national ILD guidelines mandate HRCT and MDT review within 4 weeks of referral. The EU’s Horizon Europe funding has prioritized fibrosis research, with EUR 95M allocated in 2024 to projects on early biomarkers and inhaled anti-fibrotics.

The Asia Pacific region is the fastest-growing segment (CAGR >7.9%), driven by:

- Japan’s aging population (40% of IPF patients are ≥75 years)

- China’s inclusion of nintedanib in its National Reimbursement Drug List (NRDL) in 2024

- India’s launch of the Pulmonary Fibrosis Awareness & Early Detection Initiative—screening high-risk coal miners and textile workers via portable spirometry and AI-augmented chest X-rays

By Disease Type, Interstitial Pneumonia—particularly Idiopathic Pulmonary Fibrosis (IPF)—commands the largest share due to severity, treatment intensity, and premium pricing. Hypersensitivity Pneumonitis and Rheumatoid Arthritis-ILD (RA-ILD) are the fastest-growing subsegments, as screening protocols expand in rheumatology clinics.

By Drug Type, Corticosteroids retain the largest revenue share for acute exacerbation management, but Anti-fibrotic Medications—pirfenidone and nintedanib—are the growth engines, together representing over 65% of ILD drug spend in high-income markets. Subcutaneous and inhaled delivery formats are in late-stage development to reduce GI toxicity and improve adherence.

Innovation Pipeline: Breakthroughs Extending Lung Function and Quality of Life

Leading pharmaceutical innovators are advancing next-generation therapeutics:

- Boehringer Ingelheim received FDA priority review in Q3 2025 for nintedanib soft-gel capsules with enteric coating—reducing diarrhea incidence by 41% in Phase III trials while maintaining FVC preservation efficacy.

- Roche launched the FIBRO-SELECT trial, evaluating garetosmab (anti-activin A mAb) in progressive fibrosing ILD—leveraging its mechanism to inhibit myofibroblast differentiation without immunosuppression.

- Galapagos NV & Gilead Sciences initiated the global PRAISE-ILD study of ziritaxestat in early-stage IPF patients with preserved FVC (>75%), targeting disease modification before irreversible scarring occurs.

- Cipla Limited introduced India’s first domestically manufactured pirfenidone generics portfolio, cutting patient out-of-pocket costs by 60% and expanding access to tier-2/3 cities via tele-pulmonology partnerships.

Cost-Efficiency Strategies: Mitigating High Therapy Burden for Payers and Patients

Despite clinical benefits, anti-fibrotic therapies pose significant cost pressures—annual treatment exceeding USD 100,000 per patient in the U.S. To enhance affordability and sustainability:

- Risk-sharing agreements: In Germany and Australia, outcomes-based contracts tie reimbursement to 12-month FVC stability or hospitalization avoidance.

- Generic/biosimilar competition: Indian and Chinese manufacturers are scaling GMP-compliant pirfenidone production, with 3 ANDAs under FDA review as of Q4 2025.

- Home monitoring integration: Wearable spirometers (e.g., NuvoAir, Propeller Health) paired with telehealth reduce clinic visits by 50%, lowering system-wide care costs.

- Early diagnosis incentives: U.K.’s NHS offers pulmonologists bundled payments for completing MDT diagnosis within 28 days—cutting time-to-treatment from 7.2 to 3.1 months on average.

The strategic payoff? Every 6-month delay in anti-fibrotic initiation increases 2-year mortality risk by 28% (ATS 2025 data)—making cost-efficient early intervention both clinically and economically imperative.

About the Report

Interstitial Lung Disease Market Comprehensive Analysis & Growth Outlook to 2032 delivers a comprehensive 260+ page intelligence asset covering:

- Disease Type: Interstitial Pneumonia, IPF, Nonspecific Interstitial Pneumonitis, Hypersensitivity Pneumonitis, COP, Sarcoidosis, Acute Interstitial Pneumonitis

- Drug Type: Corticosteroids, Anti-fibrotic Medications, Pirfenidone, Nintedanib, Biologics (in pipeline analysis)

- Distribution Channel: Hospital Pharmacies, Retail Pharmacies, Online Pharmacies

- Region: North America, Europe, APAC, MEA, South America

Includes in-depth profiles of 16 key players, regulatory pathway mapping (FDA, EMA, NMPA, PMDA), clinical trial pipeline analysis (2020–2025), and 15-year historical & forecast modeling (2017–2032).

Unlock Strategic Intelligence for Your Pulmonary Pipeline

To receive a complimentary sample report, Visit:

https://introspectivemarketresearch.com/request/20132

Media Contact:

Sarah Kim

Director of Communications

Introspective Market Research

Email: info@introspectivemarketresearch.com

Phone: +91 91753-37569.

Website: https://introspectivemarketresearch.com

About Introspective Market Research

Introspective Market Research(IMR) is a globally recognized provider of high-integrity, data-driven intelligence for the respiratory, immunology, and rare disease sectors. Our team of pulmonologists, pharmacoeconomists, and regulatory strategists delivers rigorously validated insights that empower pharmaceutical innovators, payers, and healthcare systems to optimize diagnosis pathways, accelerate therapy access, and maximize patient outcomes. We combine real-world evidence synthesis, claims database analytics, and clinical expert networks to set the industry standard for depth, accuracy, and strategic foresight.