Global Panic Attack Treatment Market Set to Surge to USD 8.66 Billion by 2032, Driven by Rising Mental Health Awareness and Digital Therapeutics Adoption

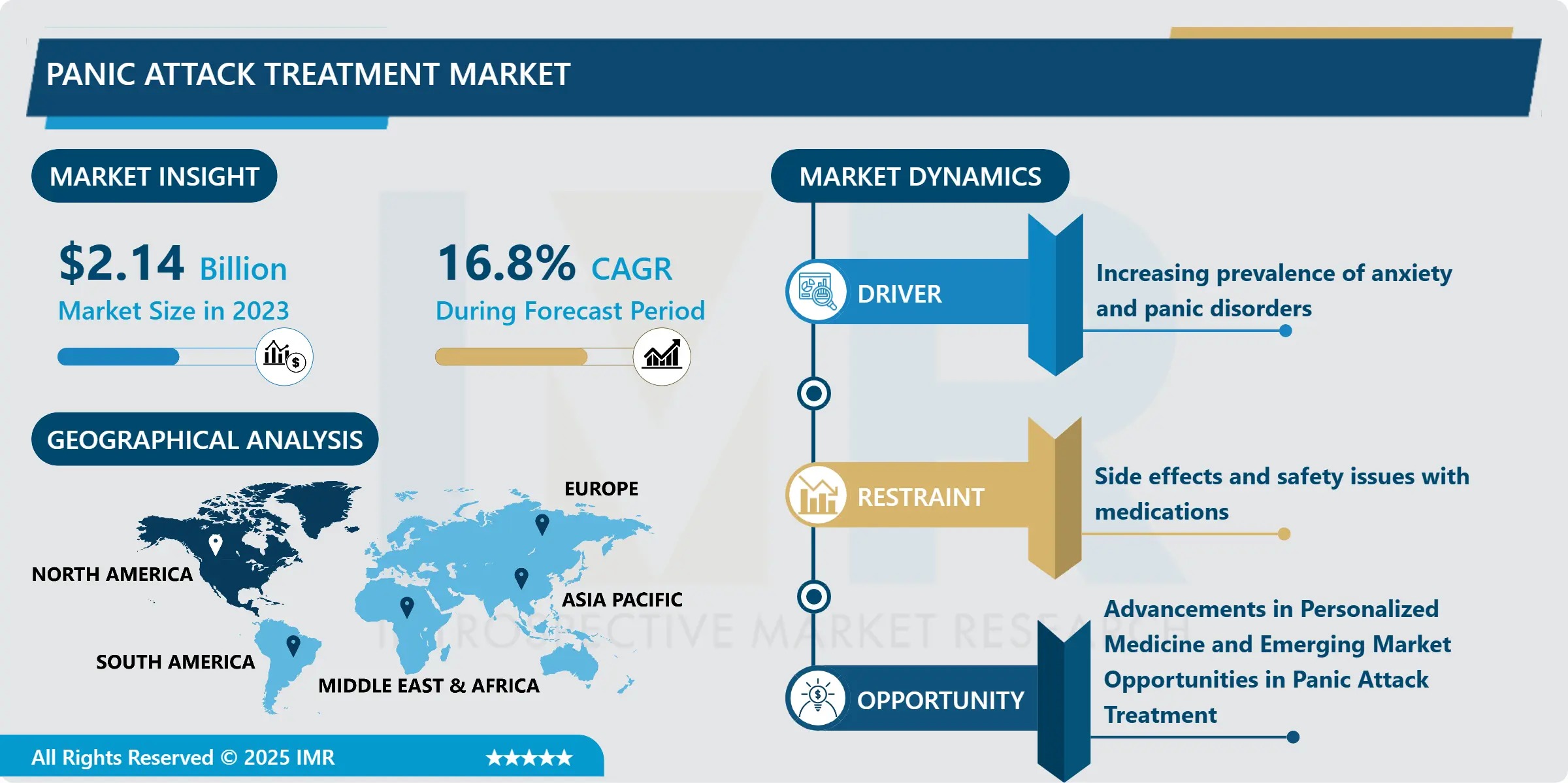

The Global Panic Attack Treatment Market is undergoing a transformative expansion, projected to grow from USD 2.14 billion in 2023 to USD 8.66 billion by 2032, recording a robust compound annual growth rate (CAGR) of 16.80% between 2024 and 2032, according to a new report by Introspective Market Research. This unprecedented growth is propelled by surging prevalence of anxiety disorders, intensified public and clinical focus on mental wellness, and rapid adoption of innovative, non-stigmatizing care models—including cognitive behavioral therapy (CBT) apps, telepsychiatry, and pharmacogenomic-guided therapeutics.

As mental health transitions from peripheral concern to central pillar of holistic healthcare, panic attack treatment is emerging as a high-growth, high-impact segment within the broader neuropsychiatric therapeutics space. Evolving reimbursement frameworks, government-led awareness initiatives, and strategic alliances between pharma and digital health innovators are accelerating market maturation—especially in high-income economies where early diagnosis and multimodal intervention are becoming standard of care.

Quick Insights: Panic Attack Treatment Market Snapshot (2023–2032)

- 2023 Market Value: USD 2.14 Billion

- 2032 Projected Value: USD 8.66 Billion

- Forecast CAGR (2024–2032): 16.80%

- Dominant Drug Class: Antidepressants (especially SSRIs)

- Largest Route of Administration: Oral (tablets, capsules, syrups)

- Leading Region: North America

- Key Players: Pfizer Inc., Eli Lilly and Company, GlaxoSmithKline plc, AstraZeneca, Johnson & Johnson, H. Lundbeck A/S, Teva Pharmaceutical Industries Ltd.

- Emerging Modality: Digital therapeutics & AI-enabled anxiety monitoring wearables

What’s Fueling This Surge? Innovation Meets Accessibility

How are psychotherapy, precision medicine, and digital disruption converging to redefine panic disorder management?

The answer lies in a threefold shift:

- Democratization of Evidence-Based Psychotherapy: Cognitive Behavioral Therapy (CBT), long considered the gold standard for panic attack intervention, is now being delivered via FDA-cleared mobile apps and virtual platforms—offering on-demand, stigma-free access. Platforms integrating real-time biofeedback, mood tracking, and clinician-guided modules are significantly improving engagement and adherence.

- Rise of Personalized Pharmacotherapy: Breakthroughs in pharmacogenomics are enabling clinicians to match patients with antidepressants or anxiolytics based on genetic metabolism profiles—reducing trial-and-error dosing and minimizing adverse effects. Companies like Lundbeck and Eli Lilly are investing in companion diagnostics to support targeted SSRI and SNRI deployment.

- Integration into Primary Care Infrastructure: With WHO and national health agencies advocating for mental health parity, panic attack screening and stepwise treatment pathways are being embedded into routine primary care—driving earlier intervention and better long-term outcomes.

“Panic disorder is no longer treated in silos,” says Dr. Evelyn R. Torres, Principal Consultant at Introspective Market Research. “We’re witnessing a paradigm shift toward integrated, patient-centric care models—where a wearable detecting HRV spikes triggers a just-in-time CBT module, followed by a telehealth consult and, if needed, a genomics-informed prescription. This convergence is not only improving clinical efficacy but also dramatically lowering the total cost of care by preventing ER visits and chronic disability. The next frontier lies in predictive analytics: identifying at-risk individuals before the first full-blown panic episode.”

Regional Dynamics: North America Anchors Growth; Emerging Markets Offer Untapped Potential

North America continues to dominate the panic attack treatment market, accounting for the largest revenue share in 2023. The U.S. remains the epicenter—bolstered by high diagnosis rates, comprehensive insurance coverage (including Medicare Advantage mental health expansions), and one of the world’s most active digital health ecosystems. Telepsychiatry adoption surged post-pandemic and remains entrenched, with over 62% of outpatient anxiety clinics now offering hybrid (in-person + virtual) care.

Europe follows closely, with Western Europe—led by Germany, the UK, and France—leveraging universal healthcare systems to scale access to guideline-recommended treatments. Eastern Europe shows accelerated growth potential, driven by EU-funded mental health modernization programs.

Meanwhile, the Asia Pacific region is the fastest-growing market segment. Countries like India, China, and South Korea are witnessing a dual catalyst: rising urban stressors (corporate burnout, academic pressure) and government-backed mental health digitization (e.g., India’s National Tele-Mental Health Program). Though stigma remains a barrier, smartphone penetration and AI-driven vernacular therapy apps are accelerating outreach.

Segmentation Spotlight: Antidepressants Lead, Oral Delivery Prevails

The antidepressants segment commands the largest share within drug class segmentation—primarily due to the widespread first-line use of Selective Serotonin Reuptake Inhibitors (SSRIs) such as sertraline and escitalopram, which balance efficacy with favorable safety profiles. Tricyclic antidepressants (TCAs) and benzodiazepines remain in use for refractory cases but face declining preference due to dependency and side-effect concerns.

By route of administration, the oral segment dominates, thanks to patient preference for self-administered, non-invasive options. Tablets and capsules offer dosing flexibility, cost efficiency, and strong supply-chain maturity. However, innovations in fast-dissolving oral films and sustained-release formulations aim to improve compliance and reduce peak-trough fluctuations.

Distribution channels reflect evolving consumer behavior: while hospital and retail pharmacies remain critical, online pharmacies are gaining traction—especially among younger demographics seeking discretion and convenience. E-prescribing integrations and direct-to-consumer telehealth prescribing models are further blurring channel boundaries.

Breakthroughs & Strategic Moves by Industry Leaders

- Pfizer Inc. recently expanded its neuroscience pipeline with a Phase II trial of a novel serotonin modulator designed specifically for panic-agoraphobia spectrum disorders, featuring reduced sedation risk.

- H. Lundbeck A/S partnered with a U.S.-based digital therapeutics firm to co-develop a CE-marked CBT app integrated with wearable biosensor data for real-time panic escalation alerts.

- Eli Lilly launched a pharmacogenomic testing bundle—offering CYP2D6/CYP2C19 genotyping alongside its SSRI portfolio to optimize dosing in primary care settings.

- Johnson & Johnson’s Mindstrong Health collaboration is piloting a scalable, AI-coached mobile intervention in Medicaid populations, targeting early panic symptom interception.

Cost Pressures and Pathways to Efficiency

Despite growth, the market faces reimbursement headwinds—particularly for long-term psychotherapy and novel digital therapeutics lacking HCPCS billing codes. To enhance cost-efficiency:

- Bundled care models (e.g., “anxiety episode management” packages covering assessment, 12-week CBT, and 6-month med monitoring) are being piloted by integrated delivery networks.

- Generics penetration in SSRIs and older benzodiazepines has markedly reduced per-patient drug costs—though brand innovators counter with value-based pricing tied to adherence and remission metrics.

- Preventive digital tools offer high ROI: early data shows CBT apps can reduce relapse hospitalizations by up to 34%, translating to ~USD 2,800 annual savings per patient.

Benefits of Market Expansion Extend Beyond Revenue

Wider access to effective panic attack treatment correlates strongly with improved workplace productivity, reduced cardiovascular comorbidity, and lower rates of substance misuse. Employers are increasingly covering digital mental health benefits—recognizing panic disorder as a top driver of presenteeism. Public health campaigns normalizing help-seeking behavior (e.g., #NoMoreSilentAttacks) further amplify market reach while reducing societal burden.

About the Report

“Panic Attack Treatment Market Analysis, Share, and Future Forecast (2024-2032)” provides a granular analysis of therapeutic modalities, regional adoption curves, regulatory shifts, and emerging technology integrations. It includes strategic profiles of 12+ key players, 5-year revenue forecasts by segment, and proprietary heat-mapping of investment hotspots.

Download a Free Sample Report or Schedule a Custom Briefing

Healthcare stakeholders, investors, and policymakers can access the full report—including detailed tables on market sizing by drug class, region, and distribution channel—via the following links:

🔗 Free Sample Report: https://introspectivemarketresearch.com/request/20115

About Introspective Market Research

Introspective Market Research(IMR) is a premier global provider of syndicated and custom market intelligence across healthcare, life sciences, and advanced technologies. Our analyst team combines deep domain expertise with rigorous primary research methodologies to deliver actionable insights—helping clients navigate disruption, identify white-space opportunities, and shape evidence-based strategy. All reports undergo independent validation and include dynamic forecasting models updated quarterly.

Media Contact

Sarah K. Mitchell

Head of Corporate Communications

Introspective Market Research

Email: info@introspectivemarketresearch.com

Phone: +91 91753-37569.

Website: https://introspectivemarketresearch.com