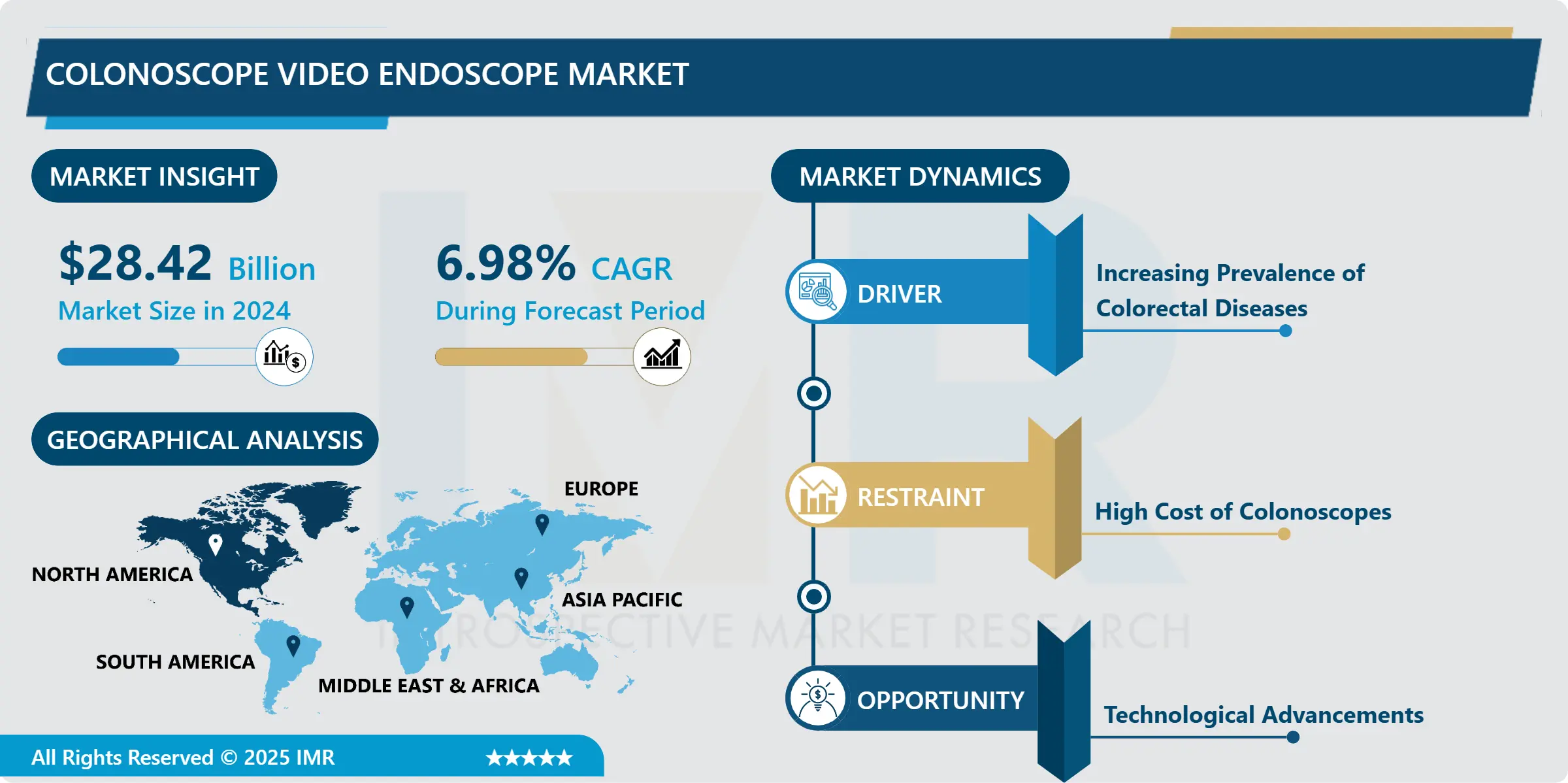

The colonoscope video endoscope market size was exhibited at USD 28.42 billion in 2024 and is predicted to be worth USD 59.70 billion by 2035, at a CAGR of 6.98% from 2025 to 2035.

Olympus (Japan)

Global market leader with the largest installed base of colonoscopy systems, known for advanced imaging platforms like EVIS X1. Strong focus on AI-driven detection, disposable distal caps, and service ecosystems that reinforce hospital loyalty.

KARL STORZ (Germany)

Renowned for precision optics and modular endoscopy systems. Strong presence in surgical endoscopy that extends into GI, offering durable video platforms with high clarity and ergonomic scope design.

Fujifilm (Japan)

A major innovator in high-resolution CMOS imaging, CAD-assisted detection, and flexible scope design. Its ELUXEO platform is a strong competitor to Olympus, especially in hospitals upgrading digital endoscopy suites.

ENDOMED (USA)

Focuses on cost-effective, reliable video endoscopy systems favored by ambulatory centers. Competitive on price with customizable configurations for mid-scale GI facilities.

Huger Endoscopy Instruments (USA)

Provides budget-friendly colonoscopes and video processors, gaining traction in emerging markets and community hospitals aiming to expand GI screening capacity.

SonoScape (China)

Fast-growing manufacturer leveraging aggressive pricing and improving imaging quality. Strong adoption in Asia and LATAM, with expanding presence in hospital procurement bids globally.

EndoChoice (USA)

Known for its Fuse® full-spectrum colonoscopy technology offering wider field-of-view. Appeals to facilities prioritizing enhanced screening capability and safety.

ANA-MED (USA)

Supplies specialized endoscopic instruments and cost-efficient colonoscopy solutions, primarily for outpatient and specialty clinics.

Pentax Medical (Japan)

Strong competitor with advanced HD visualization and therapeutic scope portfolio. Its focus on infection control and reprocessing safety boosts adoption among large GI centers.

B. Braun (Germany)

Participates indirectly via endoscopy accessories and integrated OR systems, supporting broader GI interventions with strong German engineering.

Medtronic Xomed, Inc. (USA)

Provides complementary ENT and surgical endoscopy technologies, with selective penetration in GI visualization accessories and imaging tools.

Stryker (USA)

Offers high-end imaging systems and towers, integrating GI visualization with advanced digital OR platforms. Focused on ergonomics, 4K/near-infrared, and workflow efficiency.

COOK (USA)

Strong presence in GI therapeutic devices; complements colonoscopy procedures with stents, biopsy tools, and intervention products rather than primary scopes.

Richard Wolf GmbH (Germany)

Known for precision-engineered video endoscopy systems with a strong European footprint. Preferred in specialty centers requiring high-performance imaging.

Henke-Sass Wolf GmbH (Germany)

Supplies OEM components, optical systems, and professional-grade endoscopes, supporting both branded manufacturers and hospitals with durable instruments.

XION GmbH (Germany)

Specializes in digital imaging and compact endoscopy systems optimized for outpatient and ENT/GI hybrid centers. Strong in modular video platforms.

Boston Scientific (USA)

A powerhouse in GI therapeutic tools (stents, biopsy, hemostasis). Collaborates with hospitals to integrate advanced interventions alongside colonoscopy workflows.

Endo Optiks, Inc. (USA)

Focuses on fiber-optic and micro-endoscopic visualization systems, supporting niche GI and urology procedures with unique optical designs.

Polydiagnost (Germany)

Provides versatile multi-application endoscopy systems, often chosen by cost-conscious facilities looking for adaptable platforms.

HOYA (Japan)

Parent of Pentax Medical; invests heavily in imaging optics and sensor innovation that strengthens Pentax’s colonoscope competitiveness.

Arthrex (USA)

Primarily an orthopedic endoscopy leader; offers imaging platforms applicable across specialties, occasionally used in multidisciplinary endoscopy setups.

Welch Allyn (USA)

Known for its diagnostic imaging and handheld systems; historically supports GI offices with visualization tools and light sources.

Ottomed Endoscopy (India)

Growing regional player offering economical colonoscopy systems tailored for Indian and Middle Eastern markets, focusing on accessibility and local service.

Ambu (Denmark)

Global pioneer in single-use endoscopy, including disposable colonoscopes. Strong value proposition: infection prevention, predictable costs, and reduced reprocessing burden.

Mindray (China)

Rapidly expanding medical imaging giant entering GI endoscopy with competitively priced, high-clarity video systems backed by strong after-sales networks.