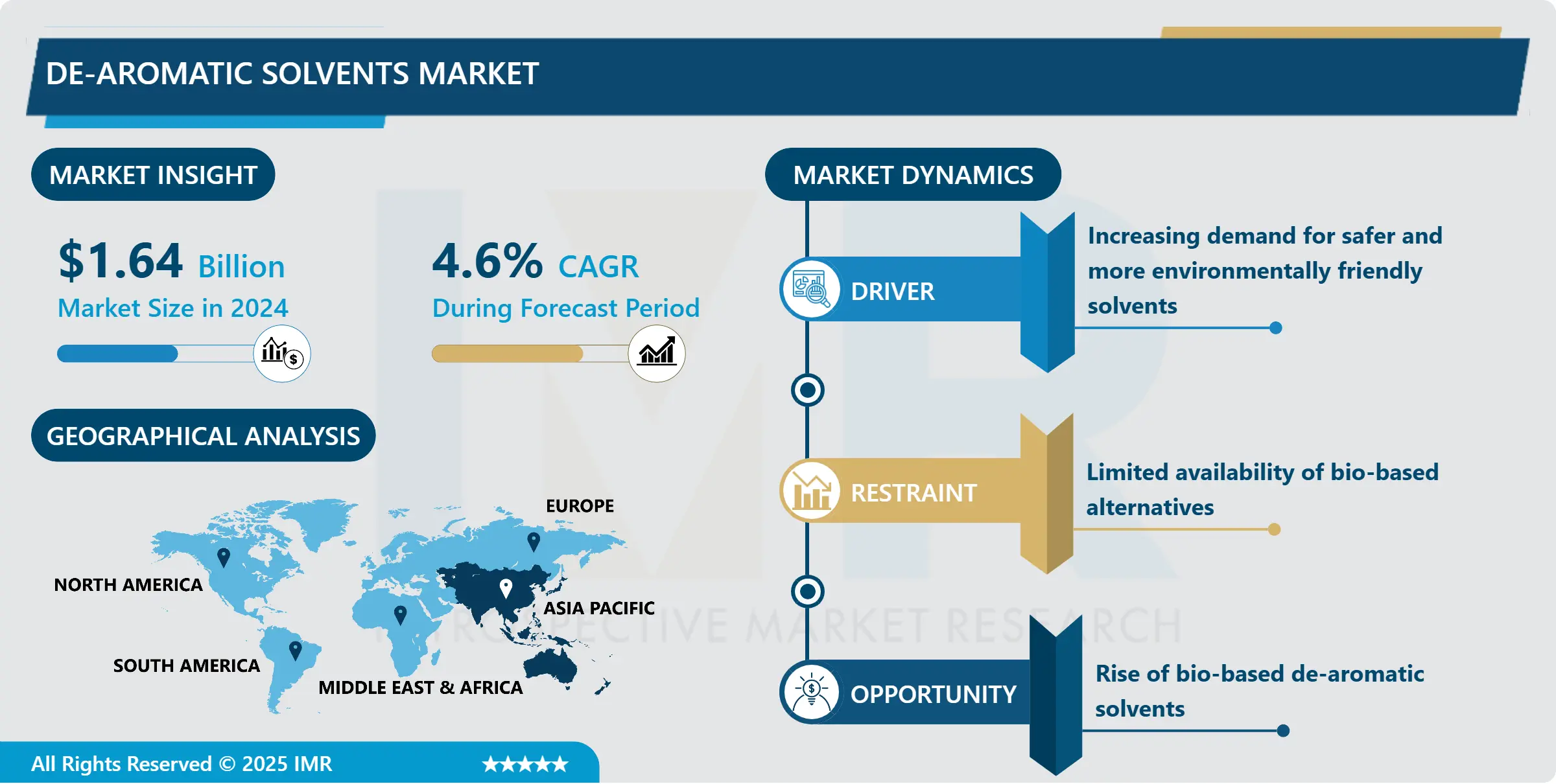

The de-aromatic solvents market size was estimated at USD 1.64 billion in 2024 and is predicted to hit around USD 2.69 billion by 2035, growing at a CAGR of 4.6% from 2025 to 2035.

Introspective Market Research (IMR) today released a comprehensive analysis of its new De-Aromatic Solvents Market Report, forecasting robust growth as industrial players pivot to greener solvent chemistry. According to IMR’s findings, the global de-aromatic solvents market is expected to expand at a compound annual growth rate (CAGR) of approximately 6.2% from the mid-2020s to 2035, underpinned by increasingly stringent environmental regulations and the rise of low-aromatic, low-odor solvent formulations.

De-aromatic solvents — hydrocarbon solvents characterized by very low aromatic content — are gaining strong traction across end-use sectors such as paints & coatings, adhesives & sealants, metalworking, and industrial cleaning. Their “cleaner” profile makes them especially attractive amid global efforts to reduce volatile organic compound (VOC) emissions and improve occupational safety.

Quick Insights

- Market Size (2025): US$ 1.64 billion

- Projected Market (2035): US$ 4.37 billion

- Forecast CAGR (2025–2035): 6.2%

- Leading Region: Asia-Pacific (especially China and India)

- Top Players: Exxon Mobil, Shell plc, TotalEnergies, Idemitsu Kosan, Neste, Raj Petro Specialities, DHC Solvent Chemie, Avani Petrochem

- Dominant Application: Paints & coatings (projected CAGR 7.4%)

- Fastest-growth Product Type: High flash-point solvents (7.1% CAGR)

Get a Sample: https://introspectivemarketresearch.com/request/878

Why Is the De-Aromatic Solvents Market Gaining Steam?

Major drivers include:

- Environmental & Regulatory Tailwinds: Regulators in North America and Europe are tightening controls on VOCs and carcinogenic solvents, and de-aromatic alternatives help companies comply.

- Sustainability Push: Increased R&D on bio-based and ultra-low aromatic grades is reshaping the product landscape.

- Industrial Demand: Key sectors — including automotive coatings, industrial cleaning, and adhesives — are rapidly substituting traditional solvents to meet safety and performance requirements.

- Emerging Markets Lead: Asia-Pacific, particularly China and India, is emerging as both the largest demand center and innovation hub as industrialization accelerates.

What Trends and Opportunities Are Unfolding?

Is sustainability redefining the dearomatic solvents value chain?

Absolutely. Leading companies are investing in circular production methods, such as bio-based feedstocks, to produce de-aromatic solvents that are not only low in VOC but also derived from renewable or recycled sources. This aligns perfectly with global ESG goals and opens pathways to differentiated products.

At the same time, the high flash-point segment prized for its stability and safety is emerging as a clear winner, particularly in metalworking and industrial operations where safety compliance is non-negotiable.

“Expert View”—Introspective Market Research Commentary

“We see the de-aromatic solvents market at a pivotal inflection point,” said Dr. Priya Narang, Principal Consultant, Introspective Market Research. “As regulatory scrutiny intensifies and customers demand safer, low-odor solvents, companies that double down on innovation—especially around bio-based or ultra-low aromatic grades will capture outsized value. Over the next decade, those who invest in R&D and sustainable feedstocks are likely to emerge as market leaders.”

Regional & Segment Breakdown

Asia-Pacific continues to dominate, supported by large-scale construction, automotive manufacturing, and tightening environmental regulations in China and India.

North America remains a major player, largely due to high regulatory standards and strong demand from aerospace, automotive, and industrial cleaning sectors.

Europe is also key, driven by green chemistry adoption and REACH-like standards.

On the product front, high flash-point solvents are growing fastest (CAGR ~7.1%) because they balance performance and safety. By boiling point, Type 3 solvents (boiling point >240 °C) are projected to lead growth thanks to their thermal stability, particularly in heavy-duty cleaning and metalworking applications.

In applications, the paints & coatings segment is projected to grow at a CAGR of ~7.4% between 2025 and 2035, as demand for low-VOC, eco-compliant coatings intensifies. Other significant applications include adhesives & sealants, industrial cleaning, and branded consumer products.

Breakthroughs From Key Players

- TotalEnergies: In a high-profile partnership with Clariter, TotalEnergies has introduced ultra-pure de-aromatic solvents made from plastic waste using hydro-de-aromatization (HDA) technology a major step toward circular chemistry.

- Neste: The company is scaling its bio-based de-aromatic solvent portfolio under the Neste RE™ brand, addressing demand from eco-conscious formulators in Europe.

- Exxon Mobil & Shell: Both are leveraging their refining-integrated models to deliver high-purity solvents that comply with REACH, EPA, and other global regulations.

Key Challenges & Cost Pressures

- Feedstock Volatility: De-aromatic solvent production remains tied to crude oil and naphtha prices, making raw material costs unpredictable.

- Capital-Intensive Production: Scaling up bio-based and HDA-based production demands significant investment in infrastructure.

- Competitive Landscape: The market is consolidated top players like Exxon, Shell, TotalEnergies, and Idemitsu command a large share raising barriers for new entrants.

- Regulatory Risks: While stricter rules are a growth driver, non-compliance risk is also real, especially in regions where environmental enforcement is uneven.

Case Study: Transition to Green Solvents

A leading European coatings manufacturer recently announced a reformulation initiative to replace its traditional aromatic solvents with high-purity de-aromatic solvents acquired from a top-tier supplier. The switch reduced VOC emissions by 30%, improved worker safety (due to lower odor and toxicity), and enhanced end-product performance — all while maintaining cost parity after accounting for lifecycle savings.

What’s Next? How Industry Players Can Seize the Moment

Introspective Market Research recommends that companies:

- Invest in R&D for bio-based and recycled feedstock to future-proof their portfolios.

- Optimize their supply chain for high flash-point, low-odor solvents, catering to safety-conscious sectors.

- Monitor geographic demand shifts, especially as Asia-Pacific continues its rapid industrialization.

- Form strategic alliances — for instance, jointly commercialize green-solvent technologies or secure sustainable feedstock sources.