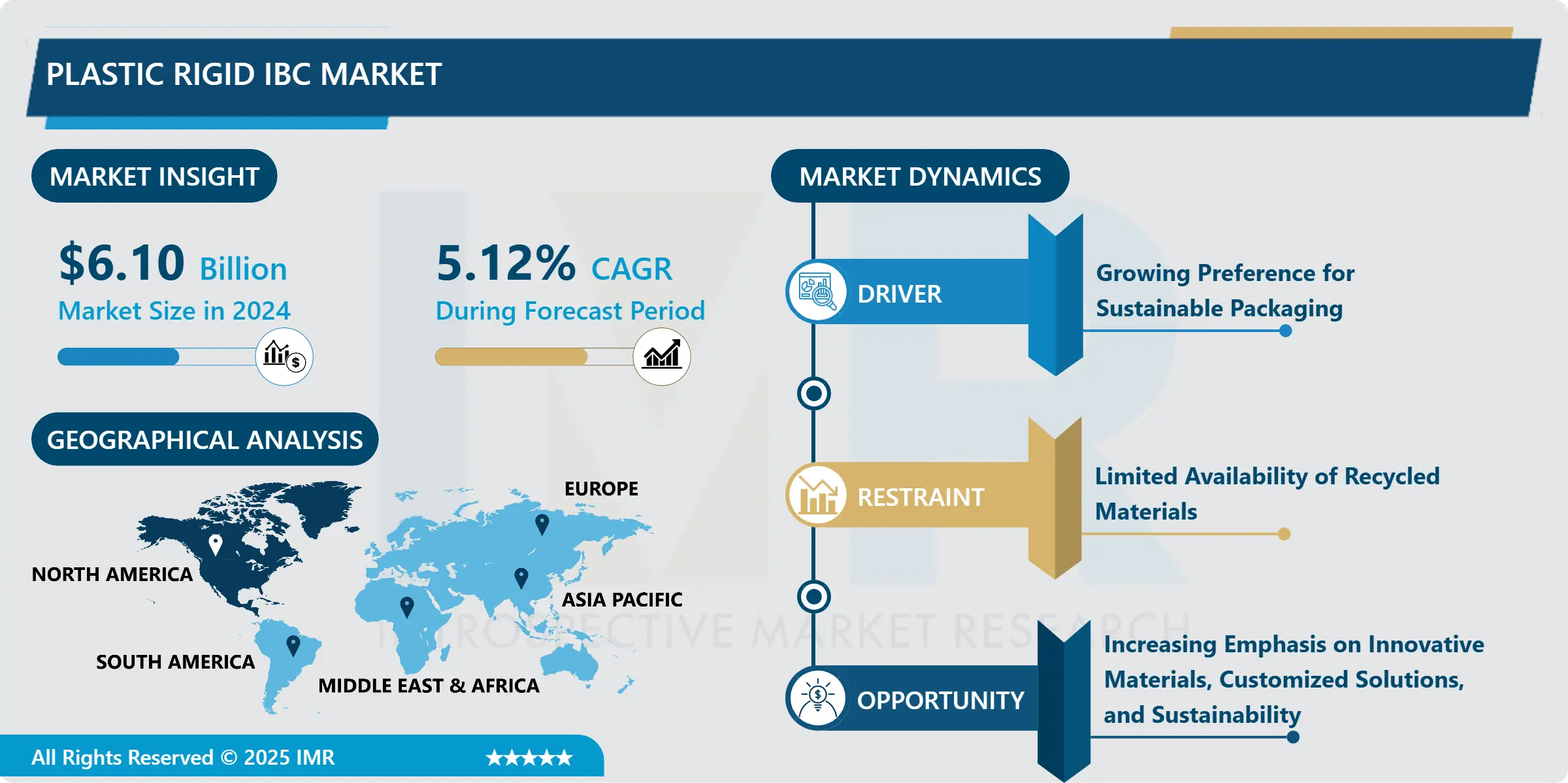

The plastic rigid IBC market size reached USD 6.10 billion in 2024 and is predicted to hit around USD 10.56 billion by 2035, growing at a CAGR of 5.12% from 2025 to 2035.

This robust growth is being propelled by several converging factors: a rising preference for sustainable packaging solutions, increasing demand from the chemical and food & beverage industries, and innovation in materials and design. As businesses increasingly prioritize environmental responsibility, plastic rigid IBCs—known for their recyclability, durability, and reusability, are emerging as key enablers of more sustainable bulk packaging strategies.

Quick Insights

- 2023 Market Size: US$ 5.08 B

- Forecast (2032): US$ 8.96 B

- CAGR (2024–2032): 4.95%

- Top Materials (by type): HDPE, LLDPE, LDPE

- Leading Capacity Segment: Up to 500 L; 501–1000 L; 1001–2000 L; Above 2000 L

- Primary End Users: Industrial Chemicals, Petroleum & Lubricants, Paints/Inks & Dyes, Food & Beverages, Pharmaceuticals, Building & Construction

- Key Regions Covered: North America; Western Europe; Eastern Europe; Asia Pacific; Middle East & Africa; South America

- Major Players: Greif (US), Mauser Packaging Solutions (US), Schütz (Germany), Snyder Industries (US), ACO Container Systems (Canada), Myers Industries (US), WERIT (Switzerland), MaschioPack (Italy), Pyramid Technoplast (Italy), Sintex (India), and others

Driving Forces Behind Market Growth

identifies several key drivers fueling the plastic rigid IBC market:

- Sustainability Imperative: Corporations are under growing pressure to reduce environmental footprints. Plastic rigid IBCs, especially when made from recyclable HDPE and other polymers, offer a compelling solution to transition away from one-time-use packaging.

- Industrial Demand: Bulk storage and transport needs are surging in sectors like chemicals, lubricants, and food & beverage. IBCs provide cost-effective, chemically resistant, and high-volume containers.

- Customization & Innovation: Manufacturers are developing tailored IBC solutions—varying in capacity, material type, and design—to meet specific end-user needs.

At the same time, restraints such as limited availability of recycled materials are slowing the pace of adoption. Despite this, opportunities are emerging around advanced materials, smart IBCs (e.g., IoT-enabled tracking), and region-specific, sustainability-driven innovations.

What’s Fueling the Opportunity?

How will sustainability and customization unlock the next wave of plastic rigid IBC growth?

As companies continue to align with ESG (Environmental, Social, Governance) goals, demand for IBCs made with recycled or bio-based resins is gaining momentum. At the same time, buyers are asking for more customized designs—optimized for capacity, chemical compatibility, stackability, and even instrumentation (for temperature, tilt, pressure). These developments represent a major opportunity in the coming years, particularly for manufacturers that can combine eco-friendly materials with intelligent design.

Plastic Rigid IBC (Intermediate Bulk Container) market Trends

- IoT & smart-tote adoption is rising — more IBCs now ship with RFID/GPS/temperature sensors and tamper-proof attachments, enabling real-time location, temperature monitoring and inventory visibility.

- Circularity pressure / recycling problems: Europe (and some other regions) is seeing major stresses in recycling infrastructure — industry reports note a sharp rise in recycling facility closures (reported ~50% increase in closures over recent years), which is forcing buyers and manufacturers to redesign for reuse and recycled-content.

- Reconditioning & reuse gaining ground — there are reports of significant reuse/adoption moves (example: U.S. manufacturers added >2.4 million new rigid IBC units in 2023–2024, with reuse/renewal programs up roughly 23% vs prior years), showing fleet refresh and circular-service models scaling.

- Strong uptake in chemical & food sectors: surveys/analyses indicate ~58% of respondents in chemical/food processing prefer IBCs for bulk liquids due to contamination control and handling efficiency.

- Logistics & space-efficiency claims: manufacturers and users report major handling/storage efficiency gains — some product/operations analyses claim up to ~75% (three-quarters) reductions in storage/transport footprint or handling steps for certain IBC configurations vs older bulk methods.

Expert Commentary

“The plastic rigid IBC market is at a transformative moment,” said Dr. Priyanka Singh, Principal Consultant at . “Customers are no longer just buying containers—they are investing in sustainability, operational efficiency, and supply-chain resilience. Companies that innovate in materials, embrace reconditioning, and incorporate tracking technologies will lead the next generation of IBC adoption.”

Expanded Regional & Segment Dynamics

North America

North America represents a mature and technically advanced market for plastic rigid IBCs, characterized by strong penetration across chemical manufacturing, pharmaceuticals, food processing, and specialty materials. The region benefits from a highly regulated environment where safety, durability, and material integrity are non-negotiable, making plastic rigid IBCs the preferred bulk packaging solution. Moreover, the presence of leading industry innovators such as Greif, Snyder Industries, and Mauser Packaging Solutions contributes significantly to product standardization, design optimization, and lifecycle enhancements. These companies are pioneering reconditioning programs, recycled-material integration, and smart-pack tracking systems, helping North American industries streamline operations while aligning with sustainability and cost-efficiency goals.

Western & Eastern Europe

Western Europe is one of the world’s most sustainability-driven packaging markets, where environmental regulations, circular economy policies, and corporate ESG commitments strongly influence procurement. Companies such as Schütz and Mauser dominate the landscape, investing heavily in recyclable HDPE solutions, multi-layer barrier technologies, and reconditioning networks that support Europe’s strict reuse mandates. Meanwhile, Eastern Europe—though somewhat less regulated—is witnessing a rapid increase in demand for IBCs due to rising industrial activity in chemicals, paints, coatings, and agricultural inputs. As these industries scale, the demand for cost-effective yet durable bulk packaging is accelerating, and interest in recycled-content IBCs is steadily growing, making Eastern Europe an emerging hotspot for sustainable packaging adoption.

Asia Pacific

Asia Pacific stands out as the fastest-expanding region, fueled by rapid industrialization, infrastructure expansion, and surging chemical, food & beverage, and construction sectors in countries like China, India, and Southeast Asia. The region’s manufacturing ecosystem is robust, enabling large-scale IBC production and cost-effective customization tailored to regional needs. Local leaders such as Sintex (India) and Shijiheng (China) are scaling up production capabilities, introducing newer resin blends, and making IBCs more accessible to small and mid-sized enterprises. Additionally, rising export activities from Asia Pacific have increased the demand for safe, stackable, and transport-friendly bulk containers, further propelling the growth of plastic rigid IBC adoption across the region.

Middle East & Africa

The Middle East & Africa market is experiencing steady growth driven by expanding oil & gas operations, petrochemical production, infrastructure development, and the rise of local manufacturing hubs. In these sectors, plastic rigid IBCs are favored for their ability to safely transport hazardous fluids, chemicals, lubricants, and construction additives across long distances and challenging environments. Reusable IBCs, in particular, offer significant advantages by lowering long-term packaging costs, reducing waste, and improving logistics efficiency. As the region moves toward greater industrial diversification and invests in downstream chemical processing, the use of durable HDPE IBCs is expected to surge in both domestic and interregional supply chains.

South America

South America’s plastic rigid IBC market is expanding as industries such as industrial chemicals, agrochemicals, food ingredients, and petroleum derivatives invest in modern bulk-handling solutions. Countries like Brazil, Argentina, and Chile are experiencing growing import–export flows, increasing the need for reliable, spill-resistant, and transport-compliant packaging systems. IBCs play a crucial role in supporting agricultural chemical distribution—one of the region’s largest demand drivers—where consistent storage, dosing accuracy, and safety are essential. With sustainability gaining traction and regional manufacturers upgrading operations, the adoption of standardized, reusable IBC systems continues to strengthen across the continent.

Segment Dynamics

Material Segmentation

The material landscape of the plastic rigid IBC market is dominated by HDPE (High-Density Polyethylene), prized for its exceptional strength, chemical resistance, and structural stability, which make it ideal for transporting hazardous and high-viscosity fluids. LLDPE (Linear Low-Density Polyethylene) plays an essential role in multi-layer IBC designs, providing superior impact absorption, flexibility, and resistance to cracking—qualities especially important for long-distance transportation and rugged environments. Meanwhile, LDPE (Low-Density Polyethylene) is preferred for lighter, more flexible containers, offering excellent clarity and ease of processing while still maintaining adequate chemical compatibility for various non-hazardous applications. Collectively, these materials allow manufacturers to tailor IBC performance to specific industrial needs, enhancing both safety and efficiency.

Capacity Segmentation

Plastic rigid IBCs are available in several capacity categories, each serving distinct industrial requirements. Up to 500-liter IBCs are widely used in food, beverage, and pharmaceutical operations where hygiene, precise dosing, and smaller batch volumes are important. The 501–1000-liter segment represents the global standard for industrial and chemical applications, balancing portability with high-volume efficiency and serving as the most popular capacity in manufacturing and logistics operations. Larger units, in the 1001–2000-liter and above 2000-liter range, are favored for bulk transport, export shipments, and long-haul storage solutions, offering maximum efficiency for large-scale chemical, lubricant, and construction material movement. These higher capacities minimize refilling cycles and reduce handling costs across supply chains.

End-User Segmentation

The industrial chemicals sector accounts for the largest share of plastic rigid IBC consumption due to the containers’ ability to safely store and transport acids, solvents, reagents, and corrosive compounds. The petroleum & lubricants industry relies heavily on IBCs for distributing oils, greases, and fuel additives, benefiting from the containers’ rugged design and leak-proof construction. In the paints, inks & dyes segment, IBCs support the movement of pigment concentrates, solvent blends, and high-density emulsions, ensuring product consistency and minimizing contamination. The food & beverages sector adopts food-grade IBCs for edible oils, sweeteners, flavorings, and bulk liquid ingredients, where hygiene and purity are crucial. Pharmaceutical manufacturers use high-purity IBCs to handle APIs, solvents, and specialty intermediates that require stringent quality and traceability controls. Finally, the building & construction industry leverages IBCs for adhesives, coatings, admixtures, and construction chemicals, where robust, mobile bulk storage can significantly enhance productivity at project sites.

Breakthroughs from Leading Players

Several major players are pushing the boundaries of the plastic rigid IBC market:

- Greif, Inc. (USA): In March 2024, Greif acquired Ipackchem Group SAS for approximately US$ 538 million, strengthening its position in industrial packaging and boosting its EBITDA margin.

- Mauser Packaging Solutions (USA/Germany): In November 2023, Mauser signed a definitive agreement to acquire Taenza, a Mexican manufacturer of steel pails and aerosol cans, expanding Mauser’s footprint in rigid metal packaging.

- Schütz (Germany), Snyder Industries (USA), ACO Container Systems (Canada), WERIT (Switzerland), MaschioPack (Italy), Pyramid Technoplast (Italy), and Sintex (India): These companies are actively innovating on IBC design, leveraging materials science, sustainability, and production scale to meet demand across geographies.

Challenges & Cost Pressures

While the market holds great promise, manufacturers and buyers face several headwinds:

- Resin Price Volatility: Fluctuating costs for HDPE and other resins—driven by raw material supply disruptions—put pressure on margins.

- Limited Recycled Material Supply: Despite demand, the availability of high-quality recycled resin remains restricted, slowing sustainable production.

- Regulatory Compliance: Stringent safety and environmental regulations require certification and testing, raising up-front expenditure.

- Logistics & Freight Costs: Bulk containers, especially large IBCs, can be expensive to transport when empty; backhaul optimization and reconditioning are key to cost efficiency.

- Competition from Alternatives: While IBCs are growing, other bulk storage media (steel drums, flexible packaging) still compete on cost, especially in regions with lower sustainability push.

Media Contact:

Priya Menon

Head of Communications

Email: media@introspectivemarketresearch.com

Website: www.introspectivemarketresearch.com