Oral Hygiene Market to Reach USD 49.88 Billion by 2032, Driven by Health Consciousness, Premiumization, and Digital-First Oral Care Innovation.

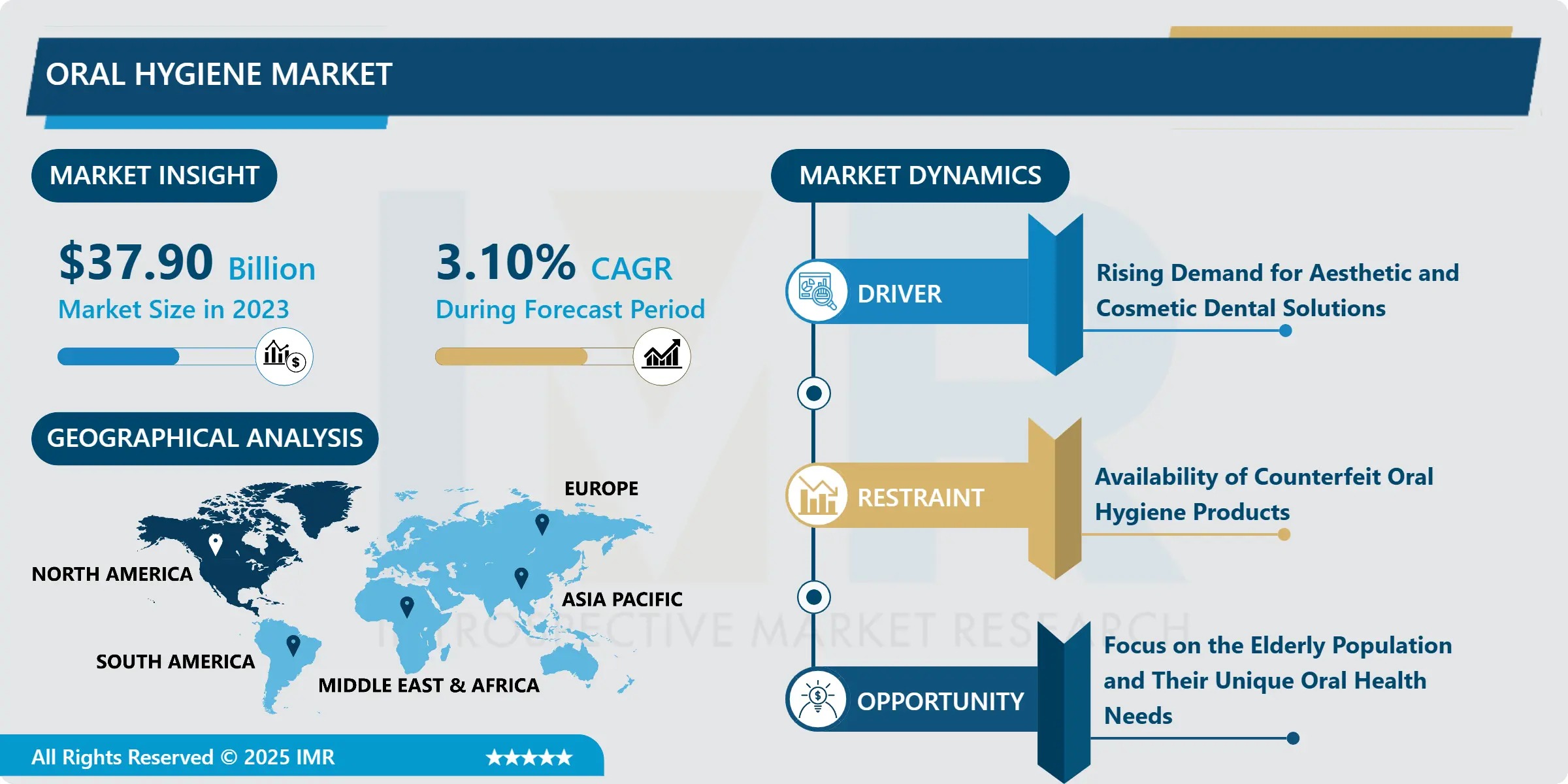

The Global oral hygiene market is projected to expand from USD 37.90 billion in 2023 to USD 49.88 billion by 2032, registering a steady CAGR of 3.10% between 2024 and 2032, according to a new report by Introspective Market Research. While growth appears modest compared to high-innovation therapeutic markets, the sector is undergoing a profound transformation—one defined not by volume spikes, but by premiumization, personalization, and preventive health integration. Key drivers include rising awareness of the oral-systemic health link (e.g., periodontitis’ association with cardiovascular disease and diabetes), surging demand for natural and sustainable formulations, and accelerating adoption of smart oral care devices powered by AI and connectivity.

As consumers globally shift from reactive dental treatment to proactive oral wellness, the market is evolving beyond basic cleaning toward holistic oral health ecosystems—where daily brushing intersects with microbiome science, aesthetic enhancement, and digital self-monitoring.

Quick Insights: Oral Hygiene Market Snapshot (2023–2032)

- 2023 Market Value: USD 37.90 Billion

- 2032 Projected Value: USD 49.88 Billion

- Forecast CAGR (2024–2032): 3.10%

- Dominant Product Segment: Toothpaste (driven by functional diversification—whitening, sensitivity, enamel repair, probiotic)

- Largest Application Segment: Daily Care (>65% share)

- Top Regional Market: North America

- High-Growth Demographics: Gen Z (aesthetic focus), Aging Population (therapeutic needs)

- Key Trends: Natural & organic formulations, smart electric toothbrushes, subscription-based oral care, influencer-led education

- Major Players: Colgate-Palmolive, Procter & Gamble, Unilever, GlaxoSmithKline, Johnson & Johnson, Kao Corporation, Lion Corporation, Church & Dwight Co., Inc., Henkel, Amway

How Is Oral Care Evolving from Routine Hygiene to Personalized Wellness?

What strategies are bridging the gap between clinical dentistry and consumer-driven prevention?

The industry is answering this with three converging innovations:

- Science-Backed Naturalization: Consumers—particularly Gen Z and millennial parents—are demanding efficacy without synthetic trade-offs. Brands are reformulating without SLS, parabens, artificial dyes, and even fluoride (in select markets), replacing them with bioactive alternatives: hydroxyapatite for remineralization, zinc citrate for antimicrobial action, xylitol for caries prevention, and postbiotic lysates for microbiome balance. Colgate’s Smile for Good and Unilever’s Zendium Probiotic+ lines exemplify this shift—delivering clinical results with clean-label transparency.

- Smart Device Democratization: Once a luxury, smart electric toothbrushes now occupy mid-tier price points (USD 60–120) and deliver data-driven brushing feedback via Bluetooth®-connected apps. P&G’s Oral-B iO Series, equipped with real-time pressure sensing, 3D teeth tracking, and AI-powered brushing coaching, has driven double-digit growth in the electric segment. Emerging entrants like Quip and Burst leverage direct-to-consumer (DTC) models and auto-refill subscriptions to capture younger, value-conscious users.

- Demographic-Specific Innovation: With over 22% of the global population projected to be aged 60+ by 2030, geriatric oral care is a high-potential frontier. Products targeting xerostomia (dry mouth), denture adhesion, root caries, and mucosal sensitivity—such as Biotène’s moisturizing rinse and GC’s Softdent line—are gaining traction. Simultaneously, child-friendly formats (edible toothpaste tablets, gamified brushing apps) are boosting early habit formation.

“Oral hygiene is no longer just about cavity prevention—it’s a gateway to whole-body wellness and self-expression,” states Dr. Priya Mehta, Principal Consultant, Consumer Health & Behavioral Insights at Introspective Market Research. “We’re seeing ‘oral health’ decouple from ‘dentistry’ in the consumer psyche. A 24-year-old may choose a charcoal-activated whitening paste not for enamel protection—but for TikTok-ready confidence. Meanwhile, a 68-year-old may prioritize a pH-balancing rinse to manage medication-induced dry mouth and reduce pneumonia risk. The future belongs to adaptive oral ecosystems—products that intelligently respond to life-stage needs, microbiome profiles, and even dietary habits. Brands that master segmentation-by-biology, not just demographics, will lead the next decade.”

Segmentation Spotlight: Toothpaste Leads, Daily Care Anchors, Premiumization Accelerates

By Product Type: Toothpaste Commands Largest Share

Toothpaste remains the market’s cornerstone—accounting for ~42% of total revenue—due to its daily use frequency and rapid innovation cycle. Sub-segments driving premium growth include:

- Whitening toothpastes (14.3% CAGR): Now integrating blue covarine, PAP (phthalimidoperoxycaproic acid), and LED-activated formulas.

- Sensitivity relief: Potassium nitrate and stannous fluoride variants dominate, with Colgate’s Sensitivity Pro-Relief holding ~18% category share.

- Enamel repair & regeneration: Hydroxyapatite-based pastes—popular in Europe and Asia—are entering U.S. mass retail, backed by clinical studies showing 3x greater remineralization vs. fluoride alone.

Toothbrushes rank second, with electric models growing 2.8x faster than manual. Sonic technology now leads over oscillating-rotating in new launches, citing gentler gum impact and superior biofilm disruption.

Mouthwash/Rinse is seeing a bifurcation: alcohol-free therapeutic rinses (e.g., chlorhexidine alternatives like cetylpyridinium chloride) for gum health, and cosmetic “fresh breath” mists for on-the-go confidence—fueled by social media culture.

By Application: Daily Care Dominates, Therapeutic Gains Ground

Daily care—routine brushing, flossing, rinsing—holds ~68% share, anchored by habitual use and wide accessibility. However, therapeutic care (for gingivitis, sensitivity, dry mouth) is the fastest-growing segment (4.9% CAGR), as consumers increasingly manage oral conditions at home post-dental consultation. Notably, cosmetic care—driven by teeth whitening strips, LED kits, and breath-freshening sprays—is surging among urban professionals, with DTC brands like Crest Whitestrips and Snow capturing significant share.

Regional Dynamics: North America Leads, Asia Pacific Accelerates

North America retains the largest market share, underpinned by high per capita spend (USD 42.70 annually), robust e-commerce infrastructure, and strong dental insurance coverage that includes preventive care subsidies. The U.S. alone contributes over 47% of global revenue, with subscription models (e.g., Quip, Burst) achieving 30%+ repeat-purchase rates.

Europe reflects a regulatory- and sustainability-driven landscape. The EU’s upcoming restrictions on microplastics (e.g., in whitening scrubs) and mandatory ingredient transparency (INCI labeling) are accelerating bio-based innovation. Germany and the UK lead in electric toothbrush adoption, while France favors natural/organic brands like Logona and Weleda.

Asia Pacific is the highest-growth region, projected to expand at 4.3% CAGR. Urbanization, rising disposable incomes, and aggressive influencer marketing are key. In India, sensitivity and whitening products show strongest uptake; in Japan and South Korea, oral beauty (hagushiru culture) drives demand for breath perfumes and tongue-coating removers. China’s post-pandemic “health-first” mindset has elevated oral care from hygiene to wellness—boosting premium imports and local R&D.

Breakthroughs & Strategic Moves by Industry Leaders

- Colgate-Palmolive launched Colgate Optic White Renewal, a PAP-based whitening toothpaste clinically proven to whiten 10x better than regular paste—without peroxide irritation.

- Procter & Gamble integrated AI coaching into Oral-B iO10, using on-handle sensors and smartphone AR to guide users through missed zones in real time—reducing plaque by 53% in 4 weeks (per clinical trial).

- Unilever expanded its Zendium probiotic line with a new variant featuring Lactobacillus reuteri, shown to inhibit S. mutans colonization and reduce gingival bleeding by 31% over 8 weeks.

- Kao Corporation introduced Sensodyne Rapid Relief Nano, a Japan-exclusive nano-hydroxyapatite toothpaste delivering sensitivity relief in 60 seconds—leveraging proprietary particle dispersion tech.

- Church & Dwight (makers of Arm & Hammer) partnered with dental AI startup Overjet to embed radiograph analytics into dentist-facing platforms, linking home care compliance with clinical outcomes for personalized product recommendations.

Cost Pressures and Pathways to Value-Driven Growth

While premiumization lifts margins, affordability remains critical for mass adoption—especially in emerging economies. Key efficiency strategies include:

- Concentrated Formats: Toothpaste tablets and dissolvable mouthwash strips reduce shipping weight/volume by up to 70%, lowering logistics costs and carbon footprint—adopted by startups like by Humankind and Denttabs.

- Refillable Systems: Electric toothbrush brands (e.g., Philips Sonicare, Oral-B) now offer replaceable brush heads with recycled plastic content and take-back recycling programs—enhancing sustainability and repeat revenue.

- Private Label Innovation: Retailers like CVS Health and Boots are launching clinically validated store brands (e.g., whitening strips with comparable efficacy to national brands at 40% lower price), expanding access without sacrificing trust.

- Preventive ROI Messaging: Brands are quantifying long-term savings: e.g., “Daily use of anti-gingivitis rinse reduces risk of periodontal surgery by 64%—saving USD 3,200+ in lifetime dental costs.”

Benefits Extend Beyond Brighter Smiles: Systemic Health, Economic, and Social Gains

Investing in oral hygiene yields cascading returns:

✔ Reduced Systemic Disease Risk: Effective plaque control lowers inflammatory burden, cutting risks of heart disease (+20% reduction in CVD events) and diabetic complications.

✔ Workforce Productivity: Oral pain costs U.S. employers an estimated USD 4.8B annually in absenteeism—preventable with accessible home care.

✔ Mental Wellbeing & Social Confidence: 76% of adults report improved self-esteem with whiter teeth and fresher breath—directly impacting social engagement and career interactions.

✔ Health Equity: Low-cost innovations like fluoride varnish strips and school-based brushing programs are narrowing oral health disparities in LMICs.

About the Report

“Oral Hygiene Market – Latest Advancement & Future Trends (2024-2032)” delivers a comprehensive analysis across product type, application, end user, and region. Highlights include:

- 10-year revenue forecasts (2017–2032) with volume analysis

- Ingredient trend mapping: rise of hydroxyapatite, postbiotics, natural antimicrobials

- DTC vs. retail channel performance benchmarks

- Regulatory impact assessment (EU microplastic ban, FDA fluoride guidelines)

- Competitive profiling of 12+ leaders, including innovation pipeline heatmaps

Download a Free Sample Report or Schedule a Custom Briefing

Brand strategists, product developers, investors, and retail executives can access the full report—including comparative market sizing tables, formulation innovation matrices, and growth opportunity dashboards—via the following links:

🔗 Free Sample Report: https://introspectivemarketresearch.com/request/20105

About Introspective Market Research

Introspective Market Research(IMR) is a global leader in consumer health, personal care, and medical device intelligence. Our research combines primary interviews with 180+ industry stakeholders, retail audit data, social sentiment analysis, and proprietary forecasting engines to deliver strategic, actionable insights. All reports include dynamic scenario modeling and are updated quarterly to reflect regulatory, technological, and behavioral shifts.

Media Contact

Anya K. Desai

Senior Director, Global Communications

Introspective Market Research

Email: info@introspectivemarketresearch.com

Phone: +91 91753-37569.

Website: https://introspectivemarketresearch.com