Global Pediatric Nutrition Market to Reach USD 6.61 Billion by 2032, Driven by Rising Parental Awareness Organic Product Demand.

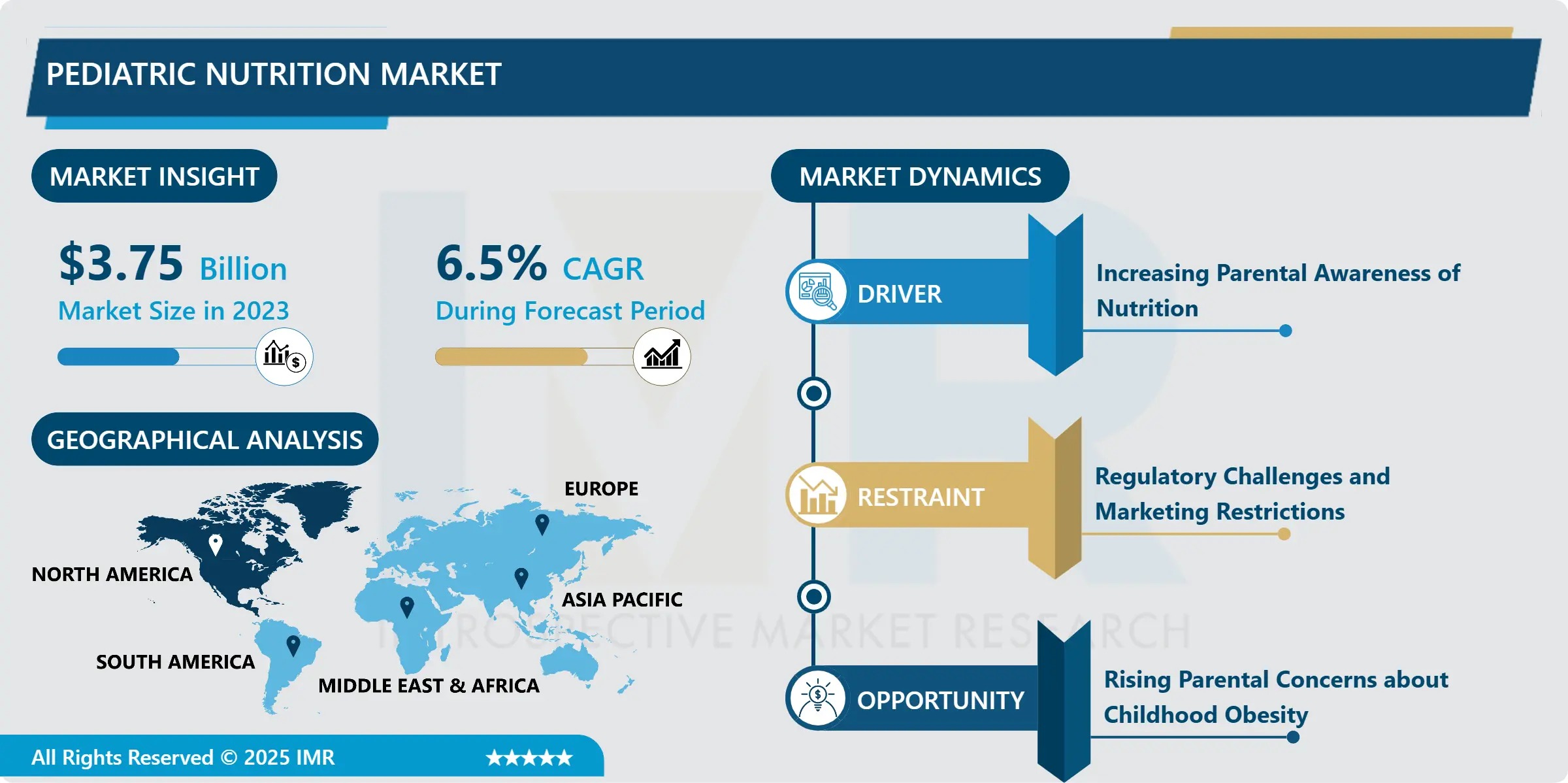

The Pediatric Nutrition Market is entering a high-impact growth phase, propelled by heightened parental vigilance around developmental nutrition, rising rates of childhood obesity and food sensitivities, and surging demand for clean-label, science-backed formulations for children aged 0–5 years. According to the latest comprehensive analysis by Introspective Market Research, the market—valued at USD 3.75 Billion in 2023—is forecast to expand to USD 6.61 Billion by 2032, growing at a steady compound annual growth rate (CAGR) of 6.5% from 2024 to 2032.

Pediatric nutrition encompasses a suite of specialized products—including infant formulas, toddler milks, fortified cereals, functional snacks, and medical nutrition therapies—designed to support optimal physical growth, neurocognitive development, immune maturation, and gut health during the critical first 1,000 days of life. With WHO data indicating that over 149 million children under five suffer from stunting globally, and rising concerns over ultra-processed diets contributing to early-onset metabolic disorders, parents, clinicians, and policymakers are increasingly prioritizing evidence-based early-life nutrition interventions.

Quick Insights: By the Numbers

- 2023 Market Size: USD 3.75 Billion

- 2032 Projected Value: USD 6.61 Billion

- CAGR (2024–2032): 6.5%

- Dominant Product Type: Infant Nutrition (accounts for largest share due to reliance on formula feeding in dual-income households and medical necessity for preterm/low-birth-weight infants)

- Largest End-User Segment: Hospitals (key channel for delivery of specialized medical nutrition to NICU, pediatric ICU, and malnutrition cases)

- Top Regional Market: North America (driven by high disposable income, regulatory frameworks supporting fortified foods, and widespread insurance coverage for therapeutic nutrition)

- Fastest-Growing Region: Asia Pacific (CAGR >7.2%, boosted by urbanization, rising middle-class spend on child wellness, and government nutrition initiatives in India and China)

- Key Players: Abbott Laboratories (USA), Nestlé (Switzerland), Danone (France), Mead Johnson Nutrition (USA), Reckitt Benckiser (UK), FrieslandCampina (Netherlands), Hain Celestial Group (USA), Hero Group (Switzerland), Arla Foods (Denmark)

Opportunity Spotlight: Can Functional, Organic, and Personalized Nutrition Solutions Reshape the Pediatric Health Paradigm?

Two macro-trends are redefining the competitive landscape: the clean-label revolution and the functionalization of everyday foods. Parents today are rejecting synthetic additives—opting instead for organic-certified, non-GMO, allergen-conscious formulas and snacks free from artificial colors, flavors, and preservatives. This has catalyzed innovation in plant-based DHA sources (e.g., algal oil), prebiotic fiber blends (HMOs, GOS/FOS), and bioavailable mineral fortification (iron, zinc, calcium chelates).

Simultaneously, functional pediatric nutrition is surging—products now target specific developmental endpoints:

- Brain & Vision: DHA + ARA + choline-enriched formulas to support synaptic pruning and retinal development

- Immunity: Synbiotic blends (probiotics + HMOs) proven to reduce incidence of respiratory and GI infections

- Gut Comfort: Partially hydrolyzed proteins and low-lactose formulations for colic, reflux, and CMPA management

Emerging digital tools—such as AI-powered growth trackers and microbiome-informed feeding apps—are laying the groundwork for personalized nutrition plans, where product selection aligns with a child’s genetic predispositions, feeding tolerance, and developmental milestones.

“Pediatric nutrition is no longer just about caloric adequacy—it’s about developmental precision,” says Dr. Fiona Chen, Principal Consultant, Early-Life Nutrition & Developmental Health Practice at Introspective Market Research. “We’re seeing a convergence of pediatric gastroenterology, immunology, and neuroscience in product design. The next frontier lies in biomarker-integrated formulations—where a simple stool or saliva test could inform real-time adjustments to a child’s nutritional regimen. Companies investing in clinical validation of cognitive and immune outcomes—not just growth metrics—will capture premium positioning and clinician trust.”

Regional Leadership & Strategic Segmentation Breakdown

North America leads in market value (38–42% share in 2023), anchored by the U.S., where over 80% of infants receive some formula supplementation. Robust reimbursement pathways for medical foods (e.g., under Medicaid’s EPSDT program), coupled with direct-to-consumer e-commerce growth (+22% YoY in 2024), are accelerating access. Canada shows strong uptake in organic toddler milks, while Mexico’s hospital segment is expanding due to public health campaigns targeting infant malnutrition.

Europe follows with mature regulatory oversight (EFSA health claims substantiation) and high HMO adoption. Germany and the UK lead in hypoallergenic formula innovation, while Nordic markets prioritize sustainability—driving demand for plant-based protein alternatives and carbon-neutral packaging.

The Asia Pacific region is the fastest-growing, with China and India together expected to account for over 50% of incremental market growth post-2027. In India, government programs like POSHAN Abhiyaan are scaling fortified complementary foods for rural communities, while urban Chinese parents drive demand for premium organic formulas—even amid tightening advertising regulations on infant nutrition.

By Product Type, Infant Nutrition dominates, with powdered formulas holding ~65% of segment revenue due to cost-efficiency and shelf stability. Liquid-read-to-feed formats, though pricier, are gaining traction in hospital and high-income home settings for infection control and convenience.

By End User, Hospitals command the largest share-particularly for preterm, surgical, and metabolic disorder cases-where products like Abbott’s Similac NeoSure and Nestlé’s Alfare are standard-of-care. Pharmacies and online retail are the fastest-growing channels, with Amazon, PharmEasy, and JD Health reporting 30%+ annual increases in pediatric nutrition SKUs.

Innovation Pipeline: Breakthroughs Bridging Science and Parent Trust

Leading players are advancing clinical and formulation excellence:

- Abbott Laboratories launched Similac Pro-Total Comfort+, the first U.S. formula with 2’-FL HMO + partially hydrolyzed whey + dual prebiotics-demonstrating 34% reduction in functional GI symptoms in a 12-week RCT.

- Nestlé Health Science introduced NAN SupremePro Organic, a certified EU-organic formula with algal DHA, lutein, and 5 HMOs-marking the company’s largest investment in clean-label R&D to date.

- Danone’s Aptamil Profutura line now includes AI-driven dosing recommendations via its MyAptamil app, syncing with smart bottles to track intake, spit-up, and stool consistency.

- Hero Group expanded its Holle Bio toddler range with region-specific variants—e.g., iron- and vitamin D-fortified Holle Bio Hirsebrei (millet porridge) for German toddlers, and zinc-enhanced Holle Bio Reisbrei (rice cereal) for Southeast Asian markets.

Cost-Efficiency Strategies: Scaling Access Without Compromising Integrity

Despite premiumization, manufacturers face margin pressure from dairy commodity volatility, stringent traceability demands, and logistics complexity for temperature-sensitive liquids. To enhance affordability and scalability:

- Localized sourcing of key ingredients (e.g., rice protein in Asia, camel milk in MENA) reduces import dependency and freight costs.

- High-shear dry-blending technologies enable uniform micronutrient dispersion in powders—cutting waste and improving batch consistency.

- Modular packaging systems (e.g., recyclable pouches inside reusable dispensers) lower material use by 25% while enhancing shelf appeal.

- Public-private partnerships-such as Nestlé’s collaboration with UNICEF in Nigeria—are co-developing low-cost, shelf-stable ready-to-use therapeutic foods (RUTFs) for malnutrition intervention.

The result? Enhanced ROI for stakeholders: every USD 1 invested in early-life nutrition yields up to USD 16 in long-term healthcare and productivity savings (World Bank, 2024).

About the Report

Pediatric Nutrition Market: Comprehensive Analysis & Market Outlook (2024-2032) delivers a 300+ page strategic intelligence asset covering:

- Product Type: Infant Nutrition, Toddler Nutrition, Medical Nutrition, Functional Snacks

- Form: Powder, Liquid, Semi-Solid

- Distribution Channel: Hospitals, Pharmacies, Online, Hypermarkets/Supermarkets

- Age Group: 0–6 months, 6–12 months, 1–3 years, 3–5 years

- End User: Hospitals, Homecare, Specialty Clinics

- Region: North America, Europe, APAC, MEA, South America

Includes full profiles of 14 key players, regulatory deep-dives (FDA, EFSA, FSSAI, NMPA), patent landscaping (2019–2025), and granular 15-year historical & forecast modeling (2017–2032).

Unlock Strategic Foresight for Your Pediatric Nutrition Roadmap

To receive a complimentary sample report, Visit:

https://introspectivemarketresearch.com/request/20142

Media Contact:

Sarah Kim

Director of Communications

Introspective Market Research

Email: info@introspectivemarketresearch.com

Phone: +91 91753-37569..

Website: https://introspectivemarketresearch.com

About Introspective Market Research

Introspective Market Research(IMR) is a globally recognized provider of high-integrity market intelligence for the life sciences, nutrition, and child health sectors. Our team of PhD nutritionists, pediatric clinicians, and regulatory specialists delivers rigorously validated, forward-looking insights that empower Fortune 500 innovators, specialty manufacturers, investors, and global health institutions to make confident, evidence-based decisions. We combine primary physician surveys, proprietary consumption databases, and AI-enhanced forecasting to set the benchmark for accuracy, depth, and strategic relevance.