Glycopeptide Antibiotics Market to Reach $4.31 Billion by 2032, Driven by Rising MRSA Infections, Hospital-Acquired Infections.

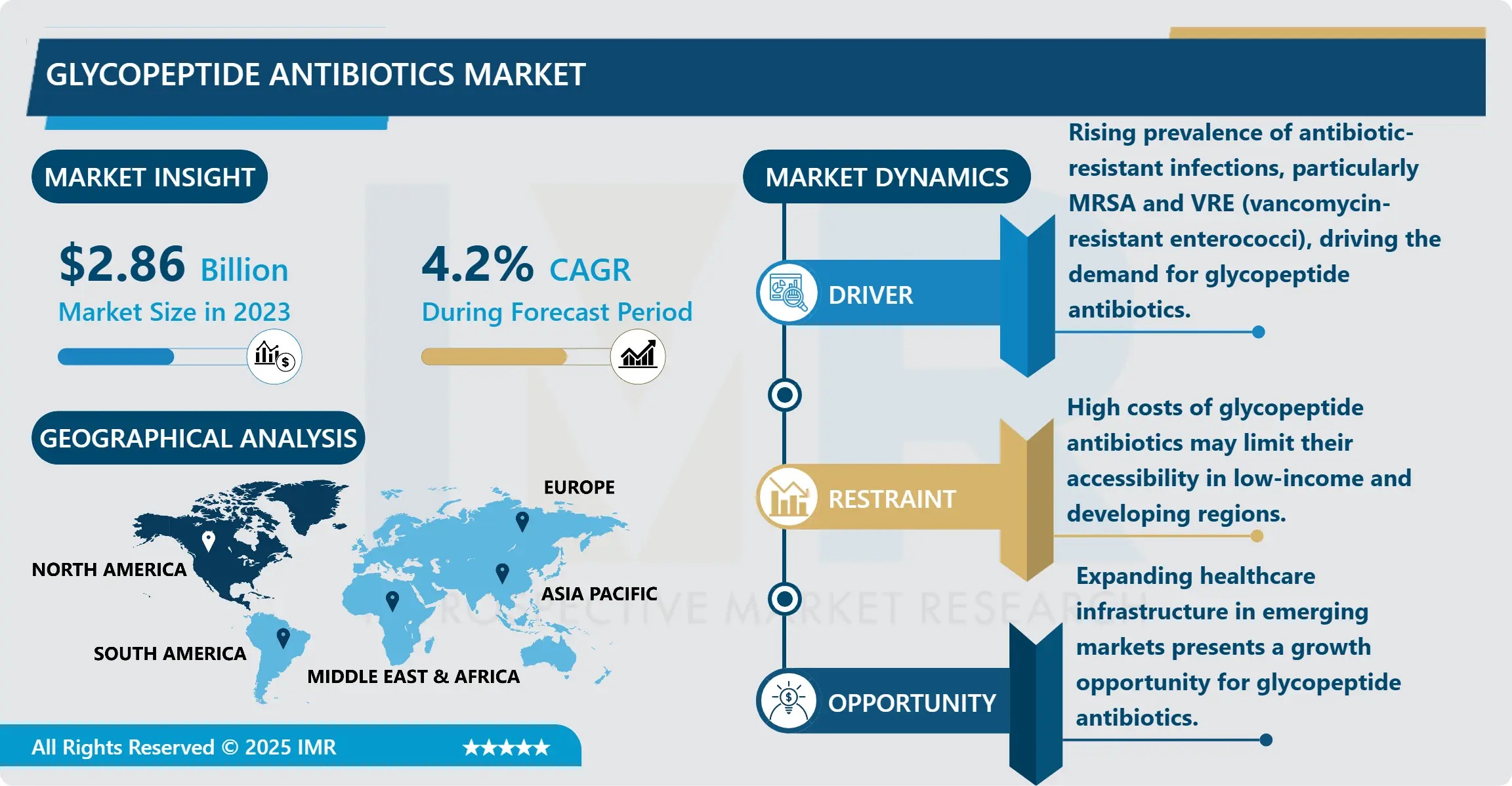

The Glycopeptide Antibiotics Market is entering a phase of measured yet critical growth, propelled by the relentless global rise in antimicrobial resistance (AMR), particularly methicillin-resistant Staphylococcus aureus (MRSA) and other multidrug-resistant Gram-positive pathogens. According to the latest comprehensive analysis by Introspective Market Research, the market—valued at USD 2.86 Billion in 2023—is on track to reach USD 4.31 Billion by 2032, expanding at a compound annual growth rate (CAGR) of 4.20% from 2024 to 2032.

Glycopeptide antibiotics—including vancomycin, teicoplanin, dalbavancin, and oritavancin—remain indispensable in the global fight against life-threatening bacterial infections, especially in hospital settings where empiric therapy for suspected MRSA sepsis, ventilator-associated pneumonia, and surgical site infections hinges on rapid, broad-spectrum Gram-positive coverage. Their unique mechanism of action—binding to the D-Ala-D-Ala terminus of peptidoglycan precursors to inhibit cell wall synthesis—makes them highly effective against resistant organisms where beta-lactams and fluoroquinolones fail.

With the WHO declaring AMR a top-10 global public health threat and projections estimating 10 million annual deaths attributable to drug-resistant infections by 2050, glycopeptides continue to serve as first-line or salvage therapy across critical care, infectious disease, and surgical specialties-ensuring sustained demand and strategic relevance in antimicrobial formularies worldwide.

Quick Insights: By the Numbers

- 2023 Market Size: USD 2.86 Billion

- 2032 Projected Value: USD 4.31 Billion

- CAGR (2024–2032): 4.20%

- Dominant Drug Type: Vancomycin (accounts for largest share due to decades of clinical validation, broad indication spectrum, and generic availability)

- Largest Application Segment: Hospital-Acquired Infections (HAIs)—including catheter-related bloodstream infections, surgical site infections, and ventilator-associated pneumonia

- Top Regional Market: North America (~42% value share in 2023), led by the U.S. due to high MRSA prevalence, advanced ICU infrastructure, and robust antimicrobial stewardship programs

- Key Players: Pfizer Inc. (USA), Merck & Co., Inc. (USA), Novartis AG (Switzerland), Roche Holding AG (Switzerland), Sanofi (France), Teva Pharmaceutical Industries Ltd. (Israel), Cipla Limited (India), Amgen (USA), Baxter International (USA), Zoetis Inc. (USA)

Opportunity Spotlight: Can Next-Generation Glycopeptides and Stewardship-Integrated Dosing Algorithms Revitalize the Class Amid Rising Resistance Concerns?

While vancomycin remains the backbone of Gram-positive coverage, therapeutic limitations—nephrotoxicity, need for therapeutic drug monitoring (TDM), and emerging vanA/vanB-mediated resistance—have accelerated innovation in the glycopeptide space. Newer agents like dalbavancin (single-dose weekly IV for acute bacterial skin and skin structure infections—ABSSSI) and oritavancin (single 1,200 mg infusion with 14-day half-life) are redefining outpatient parenteral antimicrobial therapy (OPAT), reducing hospital stays and lowering total cost of care.

Simultaneously, AI-augmented dosing platforms—such as Bayesian-guided vancomycin dosing integrated into EHRs—are optimizing exposure while minimizing toxicity. These tools leverage real-time creatinine and pharmacokinetic data to individualize regimens, aligning with CDC and IDSA-recommended stewardship best practices.

Emerging markets in Asia Pacific, Latin America, and Africa represent high-growth potential, where rising hospitalization rates, expanding critical care capacity, and national AMR action plans are driving demand for WHO-recommended “Access” and “Watch” antibiotics—including glycopeptides as essential “Reserve” agents.

“Glycopeptides are no longer just legacy drugs—they’re evolving into precision tools,” says Dr. Rajiv Mehta, Principal Consultant, Anti-Infectives & Antimicrobial Resistance Practice at Introspective Market Research. “The market is shifting from volume-based utilization to value-based deployment, where therapeutic monitoring, resistance surveillance, and outcome tracking are baked into procurement and formulary decisions. Companies investing in companion diagnostics, real-world evidence generation, and novel formulations—like inhaled vancomycin for cystic fibrosis-related MRSA—will capture premium positioning in the post-antibiotic era.”

Regional Leadership & Strategic Segmentation Breakdown

North America maintains leadership, with the U.S. contributing ~78% of regional revenue. High MRSA bloodstream infection rates (18–22 cases per 100,000 population), Medicare reimbursement for antimicrobial stewardship, and widespread use of rapid diagnostics (e.g., PCR, MALDI-TOF) enable early, targeted glycopeptide initiation. Canada and Mexico are scaling generic teicoplanin adoption for cost-sensitive outpatient programs.

Europe follows closely, with Germany, the UK, and France emphasizing stewardship-compliant use—limiting vancomycin to confirmed or high-probability MRSA cases. The EU’s Joint Action on Antimicrobial Resistance and Healthcare-Associated Infections (EU-JAMRAI II) has standardized glycopeptide prescribing across member states, curbing overuse while preserving efficacy.

The Asia Pacific region is the fastest-growing (CAGR >5.1%), fueled by:

- China’s inclusion of vancomycin hydrochloride for injection in its National Essential Medicines List (2023 revision)

- India’s National Action Plan on AMR promoting glycopeptide access in district hospitals

- Japan’s reimbursement for dalbavancin in complex skin infections—cutting hospital LOS by 3.7 days on average

By Drug Type, Vancomycin dominates due to entrenched clinical use, generic competition (~15+ FDA-approved ANDAs), and formulation versatility (IV, oral for C. difficile). However, Teicoplanin is gaining share in Europe and APAC for its once-daily dosing and lower nephrotoxicity profile. The Others segment—including dalbavancin and oritavancin—is the fastest-growing, projected to outpace 8% CAGR post-2027.

By Application, Hospital-Acquired Infections (HAIs) command the largest share, followed closely by Bloodstream Infections and Pneumonia (especially HAP/VAP). Skin and Soft Tissue Infections are the fastest-growing application, driven by the OPAT adoption of long-acting glycopeptides.

Innovation Pipeline: Breakthroughs Enhancing Safety, Convenience, and Spectrum

Leading pharmaceutical and generic manufacturers are advancing differentiated offerings:

- Pfizer launched an AUC-guided vancomycin dosing toolkit—validated across 12 academic medical centers—reducing AKI incidence by 31% while maintaining microbiological cure rates >92%.

- Cipla Limited received WHO prequalification for its teicoplanin 400mg lyophilized powder, enabling low-cost access in LMICs through UNICEF and Global Fund tenders.

- Baxter International introduced a ready-to-use vancomycin in 0.9% NaCl bag (2g/250mL), eliminating reconstitution errors and cutting nursing time by 15 minutes per dose—now used in >600 U.S. hospitals.

- Zoetis Inc. completed Phase IV trials of oritavancin in pediatric ABSSSI (ages 2–17), showing non-inferiority to vancomycin with zero infusion-related reactions—paving the way for FDA label expansion in 2026.

Cost-Efficiency Strategies: Mitigating Margin Pressure Without Compromising Stewardship Integrity

Despite generic availability, glycopeptides face pricing pressure from payers demanding AMR-compliant utilization. To balance access and sustainability:

- Lyophilization optimization (e.g., microwave-assisted drying) reduces manufacturing cycle time by 20%, cutting COGS for sterile injectables.

- Biosimilar-style interchangeability studies for generic vancomycin (e.g., comparative AUC/MIC ratio analysis) are enabling formulary substitution with confidence.

- Bundled infection pathway contracts—tying glycopeptide reimbursement to HAI reduction metrics—reward hospitals for stewardship adherence.

- Regional API sourcing: Indian and Chinese manufacturers now control >65% of global vancomycin API supply, reducing raw material costs by 25–30% vs. Western-sourced equivalents.

The strategic benefit? Each 1-day reduction in vancomycin therapy duration—enabled by rapid diagnostics and de-escalation protocols—saves ~USD 1,200 per patient in drug, monitoring, and nursing costs.

About the Report

Glycopeptide Antibiotics Market Share, Trends & Market Forecast (2024-2032) provides a rigorous 250+ page strategic assessment across 4 core dimensions:

- Drug Type: Vancomycin, Teicoplanin, Others (dalbavancin, oritavancin, telavancin)

- Application: Hospital-Acquired Infections, Skin and Soft Tissue Infections, Pneumonia, Bloodstream Infections, Others

- End User: Hospitals, Clinics, Home Healthcare, Others

- Region: North America, Europe, APAC, MEA, South America

Includes full profiles of 16 key players, patent landscaping (2019–2025), regulatory analysis (FDA, EMA, NMPA, CDSCO), and granular 15-year historical & forecast modeling (2017–2032).

Unlock Data-Driven Intelligence for Your Anti-Infectives Strategy

To receive a complimentary sample report, Visit:

https://introspectivemarketresearch.com/request/20125

Media Contact:

Sarah Kim

Director of Communications

Introspective Market Research

Email: info@introspectivemarketresearch.com

Phone: +91 91753-37569.

Website: https://introspectivemarketresearch.com

About Introspective Market Research

Introspective Market Research(IMR) is a globally recognized provider of high-integrity intelligence for the anti-infectives, hospital therapeutics, and public health sectors. Our team of ID physicians, pharmacometricians, and health policy analysts delivers rigorously validated, forward-looking insights that empower pharmaceutical innovators, hospital systems, and global health institutions to combat antimicrobial resistance with precision, equity, and impact. We combine real-world claims data, clinical trial registries, and regulatory intelligence to set the industry benchmark for depth, accuracy, and strategic relevance.